Factory and Warehouse Automation Market by Type (Articulated Robots, SCARA Robots, Cylindrical Robots, Parallel Robots and Others), by Offering (Hardware, Software and Services), by Payload Capacity (≤ 100 KG, 101-200 KG, 201-500 KG and Others), by Mobility (Stationary Robots and Mobile Robots), by Mounting type (Floor mounted, Wall-mounted and Others), and by Application (Material Handling, Cleanroom, Dispensing and others)– Global Opportunity Analysis and Industry Forecast, 2025-2030

Factory and Warehouse Automation Industry Overview

The global Factory and Warehouse Automation Market size was valued at USD XXX billion in 2024, and is expected to be valued at USD XXX billion by the end of 2025. The industry is projected to grow further, hitting USD XXX billion by 2030, with a CAGR of XY% between 2025 and 2030.

The market are experiencing significant evolution, driven by factors such as the growing and persistent challenge of labour shortages fuelling market growth, the relentless pursuit of efficient productivity, and the fundamental need for cost reduction and optimization further boosting the market. These drivers collectively contribute to the market's overall growth potential and expanding industry size by addressing workforce shortages, improving operational performance, and enabling cost-effective solutions across various sectors.

However, the market faces restraints, including the complexity of integrating new automation technologies with existing systems and infrastructure, which hinders market growth and can slow adoption due to technical challenges and high integration costs. Despite this challenge, various opportunities for industry players lie in the rise of Robotics-as-a-Service (RaaS), which creates future opportunities for the market by offering scalable and accessible automation solutions to businesses. This shift has the potential to significantly broaden market reach, foster innovation, and expand the overall market size.

The Growing and Persistent Challenge of Labor Shortages is Fuelling Market Growth

One of the most significant factors driving the adoption of factory and warehouse automation market growth is the growing and persistent challenge of labour shortages. Businesses across various sectors are finding it increasingly difficult to attract and retain a sufficient workforce for physically demanding and often repetitive tasks within manufacturing plants and distribution centers. Automation offers a compelling solution by enabling companies to maintain or even increase throughput and productivity despite a limited labour pool. Robotic systems can operate continuously without breaks and perform tasks that are ergonomically challenging or potentially hazardous for human workers. This not only addresses immediate staffing gaps but also improves workplace safety and reduces the risk of accidents.

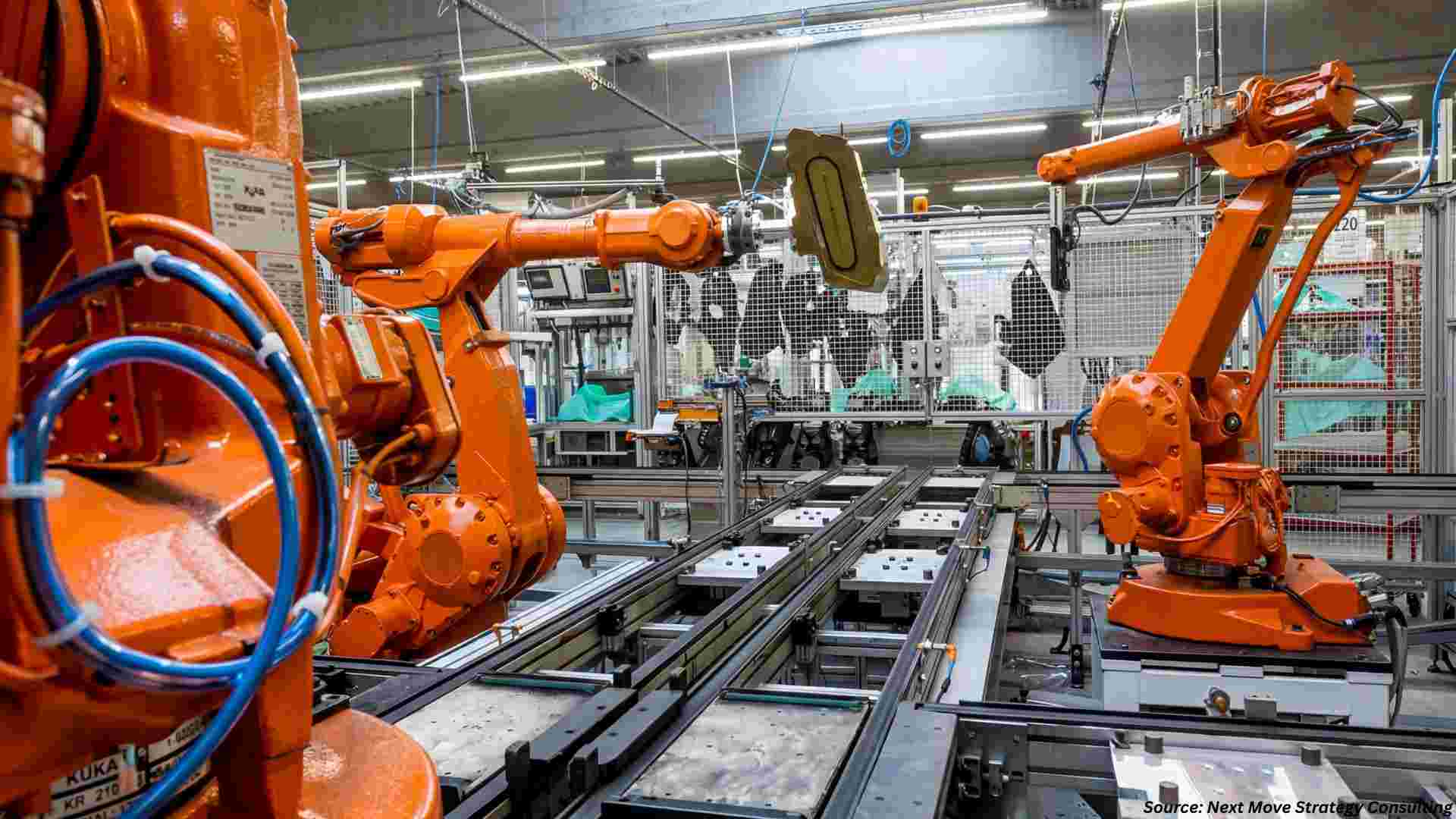

Enhanced Efficiency and Productivity Driving Market Growth in Factory and Warehouse Automation

The relentless drive for enhanced efficiency and productivity is another powerful engine propelling the factory and warehouse automation market demand. In today's fast-paced business environment, fuelled by the explosion of e-commerce and rising consumer expectations for rapid delivery, companies are under immense pressure to optimize their operations. Automation technologies, such as high-speed sorting systems, automated storage and retrieval systems (ASRS), and autonomous mobile robots (AMRs), offer significant improvements in the speed and accuracy of various warehouse processes, including receiving, put-away, picking, packing, and shipping.

According to a report published by the International Federation of Robotics in 2024, the new global average robot density reached a record 162 units per 10,000 employees in 2023, more than double the number measured (74 units) compared to the past 7 years. AI-powered robots can plan their own best routes and picking sequences, navigating autonomously in complex environments. This boost in efficiency translates directly to improved order fulfilment times, reduced operational costs, and enhanced customer satisfaction.

Cost Reduction and Operational Optimization through Industry 4.0 is Driving Market Growth in Factory and Warehouse Automation

The fundamental need for cost reduction and operational optimization is a key driver for investment in industrial robotics, particularly within the framework of Industry 4.0. While the initial capital required for automation can be significant, the long-term savings and efficiency gains typically outweigh these upfront costs. Automation helps reduce labor costs by automating repetitive tasks and decreasing the need for human workers in certain processes. In addition, it minimizes errors, particularly in order picking, leading to fewer returns and improved process accuracy. Furthermore, automated systems enable better inventory management by ensuring precise stock control, reducing the risk of overstocking or stockouts. Leveraging Industry 4.0 technologies, such as IoT-enabled devices and advanced data analytics, manufacturers can increase throughput, enhance machine uptime, and lower operational costs. These advancements in automation not only streamline production but also boost operational performance, driving the growth of the market.

The Complexity of Integrating New Automation Technologies with Existing Systems and Infrastructure Hinders Market Growth

Despite the compelling benefits, a significant restraint and challenge in the widespread adoption of factory and warehouse automation market trend is the complexity of integrating new automation technologies with existing systems and infrastructure. Many manufacturing plants and warehouses have been operating for years, if not decades, with established systems for enterprise resource planning (ERP), warehouse management (WMS), and various machinery controls. Integration challenges can arise due to incompatible software platforms, different communication protocols, and the sheer complexity of mapping data flows across various systems. Overcoming these hurdles often requires significant technical expertise, time, and investment in middleware, APIs, or even complete system overhauls in some cases.

The Rise of Robotics-as-a-Service (RaaS) Creates Future Opportunities for the Market

A significant opportunity for industry players to address the cost and flexibility challenges is the expansion of Robotics-as-a-Service (RaaS) models. This business model offers companies the ability to deploy robotic automation solutions without the large upfront capital investment associated with purchasing robots outright. Instead, customers pay a subscription fee that typically covers the hardware, software, maintenance, and updates. This pay-as-you-go approach lowers the initial barrier to entry, making automation more accessible to a wider range of businesses, including smaller companies and those hesitant to make significant capital commitments. The rise of RaaS has the potential to accelerate the adoption of warehouse and factory automation by mitigating financial risks and offering a more agile and adaptable solution for businesses seeking to enhance their operations.

Market Segmentations and Scope of the Study

The factory and warehouse automation market report is segmented on the basis of type, offering, payload capacity, mobility, mounting type, application, end user, and region. On the basis of type, the market is divided into articulated robots, SCARA robots, cylindrical robots, Cartesian/linear robots, parallel robots, collaborative robots, autonomous mobile robots (AMRs), automated guided vehicles (AGVs), and other robots. Autonomous mobile robots (AMRs) are further segmented into tow vehicle, tug vehicle, unit load vehicle, pallet truck, forklift vehicle, and other types. Automated guided vehicles (AGVs) are further segmented into laser guidance, magnetic guidance, optical tape guidance, vision guidance, and others. On the basis of offering, the market is classified into hardware, software, and services. The software segment is further divided into robot control software, vision & perception software, warehouse management system (WMS), warehouse execution system (WES), warehouse control system (WCS), and other software. On the basis of payload capacity, the market is segmented into ≤ 100 KG, 101-200 KG, 201-500 KG, 501-1000 KG, 1001-2000 KG, 2001-5000 KG, and more than 5000 KG. On the basis of mobility, the market is segmented into stationary robots and mobile robots. On the basis of mounting type, the market is segmented into floor mounted, wall-mounted, ceiling mounted, and rail mounted. On the basis of application, the market is segmented into material handling, assembling & disassembling, cleanroom, dispensing, welding and soldering, pick and place, and others. On the basis of end user, the market is segmented into automotive, semiconductor & electronics, healthcare & pharmaceutical, plastic, rubber & chemicals, metal and machinery, food & beverages, e-commerce, manufacturing, and other end users. Regional breakdown and analysis of each of the aforesaid segments include regions comprising North America, Europe, Asia-Pacific, and Rest of the World (RoW).

Geographical Analysis

North America currently holds a dominant share in the global factory and warehouse automation market share, capturing the highest revenue. The warehouse automation market is driven by factors such as labour shortages and the increasing demand for faster, more accurate warehouse processes fuelled by a robust e-commerce sector. The region is seeing a rise in the adoption of robotics and autonomous mobile robots (AMRs) to address these challenges. Notably, larger facilities in North America are embracing automation, with a significant percentage of those exceeding one million square feet having already introduced AMRs. The COVID-19 pandemic also contributed to a near-shoring trend, leading to increased factory construction and a higher demand for warehouse automation solutions in the US. Companies are focusing on maximizing ROI from automation initiatives, emphasizing strategic planning and network-wide solutions.

The long-term outlook for the European factory and warehouse automation market remains positive, driven by the global trend of reducing costs and enhancing productivity. Automation technologies, such as robotic systems, ASRS, and smart inventory management, are becoming crucial for improving speed, accuracy, and operational efficiency. The market growth is fueled by the need to minimize labor costs and improve order fulfilment times. However, a key challenge lies in integrating new automation technologies with existing legacy IT systems. Many manufacturers still operate outdated infrastructures, making it difficult to adopt Industry 4.0 solutions seamlessly. Despite this, the shift towards automation provides an opportunity for manufacturers to modernize and optimize operations. Overcoming integration barriers will be vital to driving continued growth and success in the market.

The Asia-Pacific region is emerging as a powerhouse in the warehouse automation market, with countries like China, Japan, South Korea, and the ASEAN nations leading in industrial robot sales. India is also experiencing a significant warehousing boom, driven by economic growth, government focus on local manufacturing Make in India initiative, and the consolidation of warehouses post-GST implementation. This boom is fuelling unprecedented growth in demand for warehouse automation. Indian companies like Addverb are not only catering to the domestic market but are also expanding their global presence, manufacturing a large number of autonomous robots annually. The region presents substantial growth potential for warehouse automation vendors, especially as labour costs in many APAC countries are often lower, making automation a compelling solution for efficiency and scale.

The Rest of the World region encompasses various markets with different levels of automation adoption. Factors influencing automation in these regions include the maturity of their e-commerce sectors, the availability and cost of labour, and the overall economic climate. The general global trend towards seeking automation to improve efficiency, accuracy, and reduce labor reliance suggests a gradual increase in adoption across these markets as well. The increasing accessibility and affordability of sophisticated automation solutions due to technological advancements will likely further drive market growth in the Rest of the World in the coming years.

Strategic Analysis of the Companies Operating in the Market

The factory and warehouse automation industry are intensely competitive, with key players like Dematic (KION Group), Daifuku, Swisslog (KUKA), Honeywell Intelligrated, and Symbotic adopting innovative strategies to meet rising market demand for efficient logistics. Dematic and Daifuku invest in modular AS/RS and conveyor systems, while Symbotic’s 2025 Walmart robotics acquisition strengthens micro-fulfillment capabilities. Honeywell Intelligrated integrates IoT for real-time analytics, and Swisslog prioritizes AMRs to enhance flexibility, aligning with market trends toward same-day delivery. ABB’s 2024 Sevensense acquisition bolsters AI-driven robotics, and KION’s 2025 NVIDIA partnership advances autonomous systems. Amazon’s USD 25B robotics investment, achieving 25% cost reductions in test facilities, underscores automation’s role in e-commerce. Strategic partnerships, like Falcon Autotech’s 2022 Alstef Group collaboration, expand global reach. A Porter’s Five Forces analysis reveals high rivalry among leaders, moderate buyer power due to tailored solutions, moderate supplier power from specialized components, low-to-moderate entry barriers due to capital needs, and moderate substitute threats from manual systems, mitigated by automation’s efficiency. Navigating high deployment costs and cybersecurity risks, companies drive market growth through M&A, AI, and scalable robotics.

Key Benefits

-

The report provides quantitative analysis and estimations of the market from 2025 to 2030, which assists in identifying the prevailing market opportunities.

-

The study comprises a deep dive analysis of the market including the current and future trends to depict prevalent investment pockets in the market.

-

Information related to key drivers, restraints, and opportunities and their impact on the market is provided in the report.

-

Competitive analysis of the players, along with their market share is provided in the report.

-

SWOT analysis and Porters Five Forces model is elaborated in the study.

-

Value chain analysis in the market study provides a clear picture of roles of stakeholders.

Factory and warehouse Automation Market Key Segments

By Type

-

Articulated Robots

-

SCARA Robots

-

Cylindrical Robots

-

Cartesian/Linear Robots

-

Parallel Robots

-

Collaborative Robots

-

Autonomous Mobile Robots (AMRs)

-

Tow Vehicle

-

Tug Vehicle

-

Unit Load Vehicle

-

Pallet Truck

-

Forklift Vehicle

-

Other Type

-

-

Automated Guided Vehicles (AGVs)

-

Laser Guidance

-

Magnetic Guidance

-

Optical Tape Guidance

-

Vision Guidance

-

Others

-

-

Other Robots

By Offering

-

Hardware

-

Software

-

Robot Control Software

-

Vision & Perception Software

-

Warehouse Management System (WMS)

-

Warehouse Execution System (WES)

-

Warehouse Control System (WCS)

-

Other Software

-

-

Services

By Payload capacity

-

≤ 100 KG

-

101-200 KG

-

201-500 KG

-

501-1000 KG

-

1001-2000 KG

-

2001-5000KG

-

More than 5000 KG

By Mobility

-

Stationary Robots

-

Mobile Robots

-

By Mounting Type

-

Floor mounted

-

Wall-mounted

-

Ceiling mounted

-

Rail mounted

-

By Appliation

-

Material Handling

-

Assembling & Disassembling

-

Cleanroom

-

Dispensing

-

Welding and Soldering

-

Pick and Place

-

Others

By End User

-

Automotive

-

Semiconductor & Electronics

-

Healthcare & Pharmaceutical

-

Plastic, Rubbber & Chemicals

-

Metal and Machinery

-

Food & Beverages

-

E-commerce

-

Manufacturing

-

Other End User

By Region

-

North America

-

The U.S.

-

Canada

-

Mexico

-

-

Europe

-

The UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Netherlands

-

Finland

-

Sweden

-

Norway

-

Russia

-

Rest of Europe

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Indonesia

-

Singapore

-

Taiwan

-

Thailand

-

Rest of Asia Pacific

-

-

RoW

-

Latin America

-

Middle East

-

Africa

-

Key Players

-

ABB Ltd.

-

Fanuc Corporation

-

Yaskawa Electric Corporation

-

Mitsubishi Electric Corporation

-

KUKA AG

-

Kawasaki Heavy Industries

-

Seimens AG

-

Denso Wave Inc.

-

Panasonic Corporation

-

Shibaura Machine CO., LTD

-

Omron Corporation

-

Seiko Epson Corporation

-

Staubli International AG

-

Universal Robots

-

Comau S.p.A.

REPORT SCOPE AND SEGMENTATION

|

Parameters |

Details |

|

Market Size in 2024 |

USD XX Billion |

|

Revenue Forecast in 2030 |

USD XX Billion |

|

Growth Rate |

CAGR of YY% from 2025 to 2030 |

|

Analysis Period |

2024–2030 |

|

Base Year Considered |

2024 |

|

Forecast Period |

2025–2030 |

|

Market Size Estimation |

Billion (USD) |

|

Growth Factors |

|

|

Countries Covered |

28 |

|

Companies Profiled |

15 |

|

Market Share |

Available for 10 companies |

|

Customization Scope |

Free customization (equivalent up to 80 working hours of analysts) after purchase. Addition or alteration to country, regional, and segment scope. |

|

Pricing and Purchase Options |

Avail customized purchase options to meet your exact research needs. |

")

About the Author

Jayanta Das is a senior research analyst delivering high-impact market intelligence across global markets. He leads comprehensive studies covering market assessment, forecasting, competitive evaluation, regulatory review, and trend analysis. Known for his structured and methodical approach, Jayanta excels at converting complex datasets into clear, decision-ready insights for leadership teams. His work supports strategic planning through credible sourcing, analytical precision, strong validation frameworks, and well-structured, business-focused reporting that enables confident decision-making.

Jayanta Das is a senior research analyst delivering high-impact market intelligence across global markets. He leads comprehensive studies covering market assessment, forecasting, competitive evaluation, regulatory review, and trend analysis. Known for his structured and methodical approach, Jayanta excels at converting complex datasets into clear, decision-ready insights for leadership teams. His work supports strategic planning through credible sourcing, analytical precision, strong validation frameworks, and well-structured, business-focused reporting that enables confident decision-making.

About the Reviewer

Supradip Baul is an accomplished business consultant and strategist with over a decade of rich experience in market intelligence, strategy, technology, and business transformation. His work has included rigorous qualitative and quantitative analysis across multiple industries, helping clients shape investment decisions and long-term roadmaps. Earlier in his career, he was associated with Gartner, where he contributed to industry-leading reports and market share analyses. He has worked with leading global companies and holds an MBA with a dual specialization in Marketing and Finance.

Supradip Baul is an accomplished business consultant and strategist with over a decade of rich experience in market intelligence, strategy, technology, and business transformation. His work has included rigorous qualitative and quantitative analysis across multiple industries, helping clients shape investment decisions and long-term roadmaps. Earlier in his career, he was associated with Gartner, where he contributed to industry-leading reports and market share analyses. He has worked with leading global companies and holds an MBA with a dual specialization in Marketing and Finance.

At Next Move Strategy Consulting, we understand that insightful market research is the cornerstone of successful business decisions. That's why we employ a robust and multifaceted approach, combining various methodologies to deliver the most accurate and actionable data for our clients.

Research Landscape

We navigate the world of research with two primary approaches:

Qualitative Approach

Our qualitative research methodologies involve immersive techniques such as in-depth interviews, focus groups, and observational studies. By engaging directly with individuals and stakeholders, we uncover valuable insights that quantitative data alone may overlook.

Quantitative Research

In tandem with qualitative methodologies, NMSC leverages the power of Quantitative Research to provide a robust foundation of numerical insights. Through systematic data collection and analysis, we quantify patterns, preferences, and market trends, offering a comprehensive view of the business landscape.

Our quantitative research approach employs diverse tools, including surveys, experiments, and statistical modelling. These methodologies enable us to gather data from a large and representative sample, ensuring the statistical significance of our findings. By employing structured questionnaires and standardized data collection methods, we guarantee the reliability and validity of the information we present to our clients.

Quantitative research is particularly effective in measuring the prevalence of trends, assessing market size, and gauging the impact of various factors on consumer behavior. The numerical precision attained through this approach equips our clients with actionable insights, facilitating data-driven decision-making and strategy formulation.

Our Specialized Toolbox for Industry-Specific Market Research

We deploy a specialized arsenal of techniques tailored to meet your unique requirements. Here's a glimpse into our comprehensive toolbox:

Information Procurement

The stage entails acquiring market data or relevant information through various sources and methodologies.

Market Research Approach

We utilize both top-down and bottom-up approaches in market research analysis to achieve a comprehensive understanding of the market dynamics, leveraging the broad perspective of industry trends and macroeconomic factors alongside detailed insights from specific segments and individual companies.

Porters Five Forces Analysis

We conduct Porter's Five Forces analysis to evaluate the competitive landscape of an industry, providing us with insights into factors that affect profitability and strategic positioning.

SWOT Analysis

Forecasting

We utilize a forecasting model to predict future consumption by considering parameters like population, economics, regulations, market competition, drivers, constraints, technology, and pricing. We also employ statistical techniques such as multilinear regression, exponential smoothing, moving average, ARIMA, and Monte Carlo simulations for accurate predictions. In econometric forecasting, we analyzed short-term and long-term event impacts, attributing values based on regulatory frameworks, economic factors, and market events.

Speak to Our Analyst

Speak to Our Analyst

Market")

Market")