Germany Smart Display Market by Display Technology (LCD, LED, E-Paper Display, and Other Display Technologies), by Type (Standalone Smart Displays, Integrated Smart Displays, Interactive Touchscreen Displays, Transparent Smart Displays, and Other Display Types), by Display Size (Below 24 Inch, 24 Inch to 55 Inch, and Above 55 Inch), by Resolution (UHD, FHD, HD, and Others) and Others – Opportunity Analysis and Industry Forecast, 2023–2030

Industry: Semiconductor & Electronics | Lastest Edition: March 7, 2026 | No of Pages: 157 | No. of Tables: 120 | No. of Figures: 65 | Format: PDF | Report Code : SE1016

Market Definition

Germany Smart Display Market was valued at USD 453.87 million in 2022, and is predicted to reach USD 1151.8 million by 2030, with a CAGR of 10.8% from 2023 to 2030. A smart display is a technologically advanced device equipped with a touchscreen or interactive visual interface, integrated with voice recognition and artificial intelligence capabilities.

These displays serve as information hubs that can perform a variety of functions, including displaying information, controlling smart home devices. It provides visual responses to voice commands, enabling video calls, and serving as interactive tools for tasks such as scheduling, weather updates, and entertainment.

Smart displays are designed to enhance convenience, accessibility, and user interactivity in various contexts, such as homes, offices, and public spaces. These displays are utilized in various settings, including residential homes, offices, healthcare facilities, retail, education, and more.

Driving Growth: Germany's Automotive Industry Fuels Smart Display Market Surge

The German automotive industry, with giants such as Volkswagen, BMW, Daimler, and Audi, is a driving force behind the growth of the smart display market. These companies are known for their integration of advanced smart displays in vehicles, setting industry standards and sparking demand. They prioritize innovative user interfaces that enhance the driving experience, leading to the widespread adoption of smart displays in vehicles and stimulating market growth.

For instance, in August 2023, BMW partnered with Samsung and developed the display technology for its subsidiary MINI's vehicles. The MINI Interaction Unit, a circular 9.4-inch OLED display, will be centrally positioned on the dashboard of MINI cars. This high-tech display essentially functions as an intelligent computer, running on the Android-based MINI 9 operating system. It offers features, including a GPS navigation system and a smart voice assistant that enables control over music playback, message sending, route adjustments, and more.

This partnership highlights the growing importance of advanced display technology in the automotive sector. BMW and Samsung's innovation is likely to set new standards, driving the adoption of smart displays in the broader automotive industry and, by extension, stimulating the growth of the smart display market.

Revolutionizing German Homes: The Driving Force of Integrated Smart Displays in Smart Home Solutions

The surge in the smart display market in Germany is strongly propelled by the increasing demand for smart home solutions. German consumers are actively embracing smart home technologies, with a particular focus on integrated smart displays, as they seek to create interconnected environments that elevate home automation and convenience. The desire for seamless control over various aspects of home living, such as lighting, security, and entertainment, is driving the adoption of these innovative devices.

The integration of smart displays within smart home ecosystems aligns with the growing trend of creating technologically advanced and interconnected living spaces, contributing significantly to the overall expansion of the market in Germany.

Security Vulnerabilities in Smart Home Displays Restrain Market Growth

Security vulnerabilities in smart display technology represent a significant restraining factor for the smart display market. The potential for security breaches in smart displays poses a substantial risk to users. Insufficient security measures, such as weak passwords and inadequate encryption, could lead to the exposure of sensitive data. Therefore, it is imperative for manufacturers to prioritize robust security features within smart displays, including strong authentication methods and prompt vulnerability patching through regular updates.

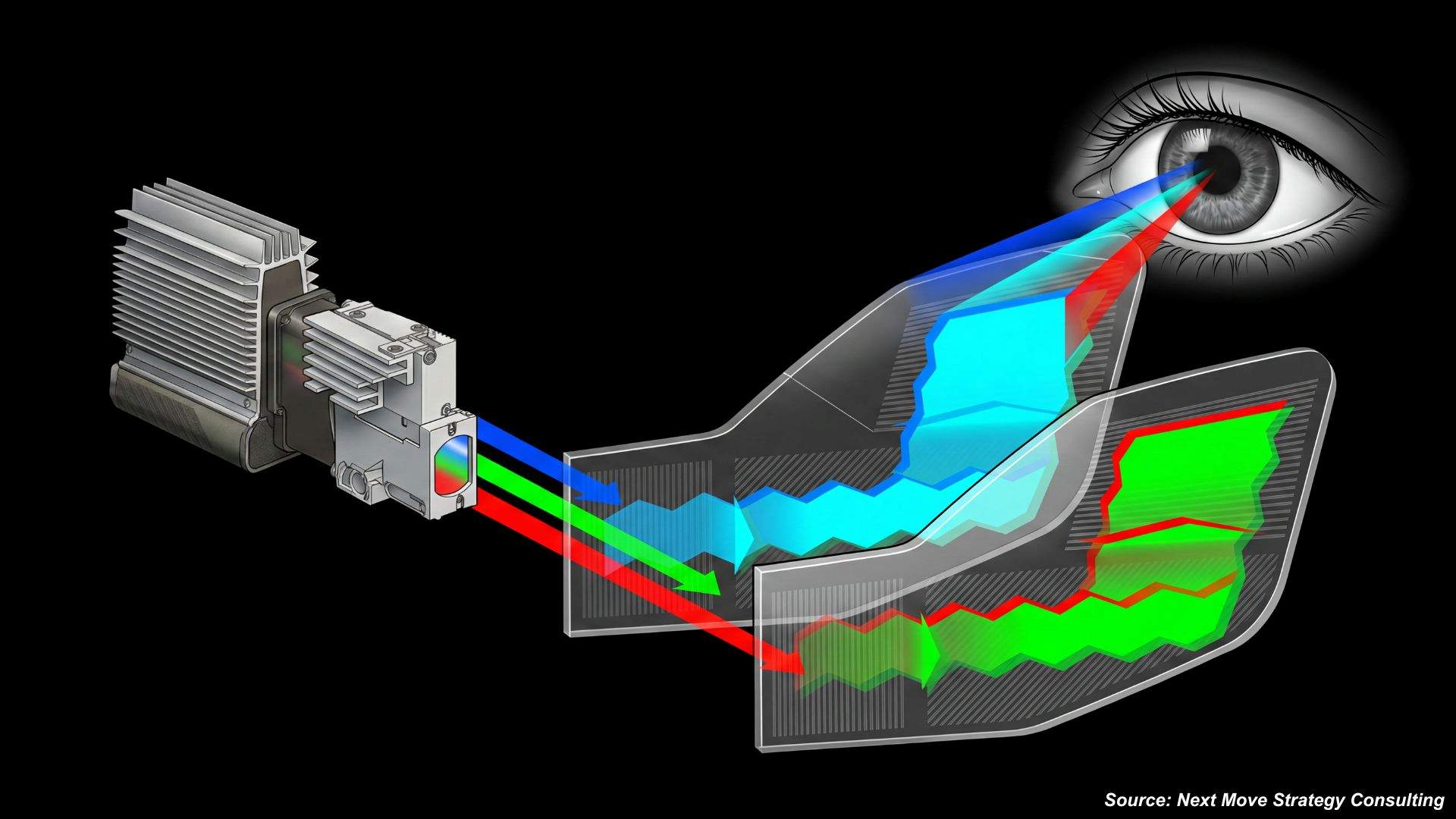

Introduction of Laser-Based Display Technology

Laser-based display technology is presenting substantial opportunities within the smart display market. Its exceptional brightness, color accuracy, long-lasting durability, and energy efficiency position it as a prime choice for diverse applications, spanning from home theaters to outdoor signage and augmented reality experiences. The extended lifespan and reliability of laser-based displays result in reduced maintenance costs and align with sustainability objectives.

As this technology becomes increasingly accessible and cost-effective, it is instigating innovation in the realm of smart displays, particularly in sectors where top-tier visual quality and energy conservation are paramount, thus broadening the market's potential for expansion.

Competitive Landscape

The Germany smart display industry includes several market players such as Siemens AG, Bosch, Hager Group, Kommatec-red.de, Samsung Electronics GmbH,LG Corporation, Sony Corporation, Google LLC, Amazon.com, Inc., Apple Inc, NEC Display Solutions Europe GmbH, Roku, Inc., AVM GmbH, Tado GmbH, DisplayHub Gmbh

Key Benefits

-

The Germany smart display market report provides a quantitative analysis of the current market and estimations through 2023-2030 that assists in identifying the prevailing market opportunities to capitalize on.

-

The study comprises a deep dive analysis of the market trend including the current and future trends for depicting the prevalent investment pockets in the market.

-

The information related to key drivers, restraints, and opportunities and their impact on the market is provided in the report.

-

The competitive analysis of the market players along with their market share in the Germany smart display market.

-

The SWOT analysis and Porter’s Five Forces model are elaborated in the study.

-

Value chain analysis in the market study provides a clear picture of the stakeholders’ roles.

Germany Smart Display Market Key Segments

By Display Technology

-

LCD

-

LED

-

E-Paper Displays

-

Other Display Technologies

By Type

-

Standalone Smart Displays

-

Integrated Smart Displays

-

Interactive Touchscreen Displays

-

Transparent Smart Displays

-

Other Display Types

By Display Size

-

Below 24 inch

-

24 inch to 55 inch

-

Above 55 inch

By Resolution

-

UHD

-

FHD

-

HD

-

Others

By Sales Channel

-

Direct Sales

-

Retailers and Distributors

-

E-Commerce Or Online Sales

By Application

-

Smart Home

-

Digital Signage

-

Automotive

-

Healthcare

-

Other Applications

Key Market Players:

-

Siemens AG

-

Bosch

-

Hager Group

-

Kommatec-red.de

-

Samsung Electronics GmbH

-

LG Corporation

-

Sony Corporation

-

Google LLC

-

Amazon.com, Inc.

-

Apple Inc

-

NEC Display Solutions Europe GmbH

-

Roku, Inc.

-

AVM GmbH

-

Tado GmbH

-

DisplayHub Gmbh

REPORT SCOPE AND SEGMENTATION:

|

Parameters |

Details |

|

Market Size in 2022 |

USD 453.87 Million |

|

Revenue Forecast in 2030 |

USD 1151.8 Million |

|

Growth Rate |

CAGR of 10.8% from 2023 to 2030 |

|

Analysis Period |

2022–2030 |

|

Base Year Considered |

2022 |

|

Forecast Period |

2023–2030 |

|

Market Size Estimation |

Million (USD) |

|

Growth Factors |

Increasing demand for smart home solutions. The widespread adoption of smart displays in vehicles. |

|

Companies Profiled |

15 |

|

Market Share |

Available for 10 companies |

|

Customization Scope |

Free customization (equivalent up to 80 working hours of analysts) after purchase. Addition or alteration to country, regional, and segment scope. |

|

Pricing and Purchase Options |

Avail customized purchase options to meet your exact research needs. |

")

About the Author

Jayanta Das is a senior research analyst delivering high-impact market intelligence across global markets. He leads comprehensive studies covering market assessment, forecasting, competitive evaluation, regulatory review, and trend analysis. Known for his structured and methodical approach, Jayanta excels at converting complex datasets into clear, decision-ready insights for leadership teams. His work supports strategic planning through credible sourcing, analytical precision, strong validation frameworks, and well-structured, business-focused reporting that enables confident decision-making.

Jayanta Das is a senior research analyst delivering high-impact market intelligence across global markets. He leads comprehensive studies covering market assessment, forecasting, competitive evaluation, regulatory review, and trend analysis. Known for his structured and methodical approach, Jayanta excels at converting complex datasets into clear, decision-ready insights for leadership teams. His work supports strategic planning through credible sourcing, analytical precision, strong validation frameworks, and well-structured, business-focused reporting that enables confident decision-making.

About the Reviewer

Supradip Baul is an accomplished business consultant and strategist with over a decade of rich experience in market intelligence, strategy, technology, and business transformation. His work has included rigorous qualitative and quantitative analysis across multiple industries, helping clients shape investment decisions and long-term roadmaps. Earlier in his career, he was associated with Gartner, where he contributed to industry-leading reports and market share analyses. He has worked with leading global companies and holds an MBA with a dual specialization in Marketing and Finance.

Supradip Baul is an accomplished business consultant and strategist with over a decade of rich experience in market intelligence, strategy, technology, and business transformation. His work has included rigorous qualitative and quantitative analysis across multiple industries, helping clients shape investment decisions and long-term roadmaps. Earlier in his career, he was associated with Gartner, where he contributed to industry-leading reports and market share analyses. He has worked with leading global companies and holds an MBA with a dual specialization in Marketing and Finance.

At Next Move Strategy Consulting, we understand that insightful market research is the cornerstone of successful business decisions. That's why we employ a robust and multifaceted approach, combining various methodologies to deliver the most accurate and actionable data for our clients.

Research Landscape

We navigate the world of research with two primary approaches:

Qualitative Approach

Our qualitative research methodologies involve immersive techniques such as in-depth interviews, focus groups, and observational studies. By engaging directly with individuals and stakeholders, we uncover valuable insights that quantitative data alone may overlook.

Quantitative Research

In tandem with qualitative methodologies, NMSC leverages the power of Quantitative Research to provide a robust foundation of numerical insights. Through systematic data collection and analysis, we quantify patterns, preferences, and market trends, offering a comprehensive view of the business landscape.

Our quantitative research approach employs diverse tools, including surveys, experiments, and statistical modelling. These methodologies enable us to gather data from a large and representative sample, ensuring the statistical significance of our findings. By employing structured questionnaires and standardized data collection methods, we guarantee the reliability and validity of the information we present to our clients.

Quantitative research is particularly effective in measuring the prevalence of trends, assessing market size, and gauging the impact of various factors on consumer behavior. The numerical precision attained through this approach equips our clients with actionable insights, facilitating data-driven decision-making and strategy formulation.

Our Specialized Toolbox for Industry-Specific Market Research

We deploy a specialized arsenal of techniques tailored to meet your unique requirements. Here's a glimpse into our comprehensive toolbox:

Information Procurement

The stage entails acquiring market data or relevant information through various sources and methodologies.

Market Research Approach

We utilize both top-down and bottom-up approaches in market research analysis to achieve a comprehensive understanding of the market dynamics, leveraging the broad perspective of industry trends and macroeconomic factors alongside detailed insights from specific segments and individual companies.

Porters Five Forces Analysis

We conduct Porter's Five Forces analysis to evaluate the competitive landscape of an industry, providing us with insights into factors that affect profitability and strategic positioning.

SWOT Analysis

Forecasting

We utilize a forecasting model to predict future consumption by considering parameters like population, economics, regulations, market competition, drivers, constraints, technology, and pricing. We also employ statistical techniques such as multilinear regression, exponential smoothing, moving average, ARIMA, and Monte Carlo simulations for accurate predictions. In econometric forecasting, we analyzed short-term and long-term event impacts, attributing values based on regulatory frameworks, economic factors, and market events.

Speak to Our Analyst

Speak to Our Analyst