Market")

Software-as-a-Service (SaaS) Market Size, Share, Growth & Forecast by Application (Horizontal SaaS: CRM, ERP, HCM, Collaboration, Analytics & Security; Vertical SaaS: Financial Services, Healthcare, Retail, Manufacturing, Education & Public Sector), Customer Size (Enterprise, Midmarket, Small Business & Consumer/Prosumer), Deployment Model (Public Multi-Tenant, and Others), and Others — Global Industry Analysis and Forecast, 2026–2035, Growing at a CAGR of 14.8% from 2026 to 2035

What Is the Software-as-a-Service Market Size?

The global Software-as-a-Service (SaaS) Market was valued at USD 315.6 billion in 2025, reflecting robust Software-as-a-Service market size growth driven by enterprise cloud adoption. The market is expected to generate revenue of USD 361.5 billion in 2026. Sustained digital transformation across enterprise and public-sector organizations, rapid AI integration within cloud-native applications, and growing adoption across emerging markets are projected to propel the market to USD 1,247.8 billion by 2035, advancing at a CAGR of 14.8% from 2026 to 2035. Key growth drivers include proliferation of usage-based and seat-based subscription models, the democratization of enterprise-grade tools for small and midmarket businesses, expansion of vertical SaaS platforms, and accelerating integration of generative AI capabilities across horizontal application categories.

|

Parameters |

Details |

|

Market Size in 2025 |

USD 315.6 Billion |

|

Market Size in 2026 |

USD 361.5 Billion |

|

Revenue Forecast in 2035 |

USD 1,247.8 Billion |

|

Growth Rate |

CAGR of 14.8% from 2026 to 2035 |

|

Analysis Period |

2025–2035 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026–2035 |

|

Market Size Estimation |

USD Billion |

|

Companies Profiled |

20 |

|

Countries Covered |

33 |

|

Market Share |

Top 10 |

Software-as-a-Service Market Overview

What Is the Software-as-a-Service Market?

Software-as-a-Service is a cloud-based software delivery model in which vendors host, manage, and continuously update applications accessible to users over the internet through subscription or consumption-based pricing. Unlike traditional on-premises software requiring capital-intensive licensing and infrastructure management, the Software-as-a-Service market enables organizations of all sizes to access enterprise-grade capabilities through flexible and scalable cloud subscriptions. The market spans horizontal applications serving cross-industry functions and vertical applications tailored for sector-specific workflows across financial services, healthcare, manufacturing, education, retail, and the public sector.

How Has the Software-as-a-Service Market Evolved Structurally?

The Software-as-a-Service market has evolved through distinct technology and commercial transformation phases. The first phase, spanning the early 2000s through 2012, was defined by the emergence of CRM and productivity cloud applications as foundational SaaS categories, pioneered by Salesforce and later Google. The second phase, from 2013 through 2020, saw rapid horizontal expansion across ERP, HCM, collaboration, security, and analytics. Our analysis indicates that the current third phase, from 2021 onward, is characterized by AI-native SaaS innovation, usage-based commercial model expansion, vertical SaaS specialization, and platform consolidation by hyperscale vendors acquiring point-solution providers.

How Do Regulations Influence the Software-as-a-Service Market?

Regulatory developments are structurally reshaping the Software-as-a-Service market across all major geographies. The EU's GDPR, the U.S. HIPAA and FedRAMP frameworks, India's Digital Personal Data Protection Act, and sector-specific mandates such as PCI DSS in financial services are compelling SaaS vendors to embed privacy-by-design, data residency options, and compliance automation into their core product architectures. Our assessment indicates that regulatory alignment is increasingly a commercial differentiator, with compliance-ready SaaS platforms commanding premium pricing and winning regulated enterprise and government procurement contracts ahead of non-compliant competitors.

How Is Technology Adoption Expanding Across the Software-as-a-Service Market?

Technology adoption across the Software-as-a-Service market is accelerating driven by the convergence of cloud-native architectures, AI/ML embedding, and no-code or low-code development tooling. NMSC's analysis indicates that generative AI capabilities, including natural language interfaces, AI assistants, and automated workflow generation, are being integrated across virtually every SaaS product category, from CRM and ERP to security and analytics platforms. Consumption-based pricing and freemium models have further lowered adoption barriers, enabling millions of small businesses and prosumer users globally to access productivity-grade SaaS tools previously reserved for large enterprise deployments.

Key Findings Across Segments, Regions, and Applications in the Software-as-a-Service Market

|

Key Takeaway |

|

By application, Horizontal Applications dominate the Software-as-a-Service market, accounting for approximately USD 221.0 billion in 2025. CRM and Customer Service is the largest horizontal sub-segment, driven by global enterprise investment in Salesforce, Microsoft Dynamics 365, and HubSpot platforms. Security and Identity is the fastest-growing horizontal sub-segment, advancing at a CAGR of 18.3% from 2026 to 2035, propelled by rising cloud security mandates and zero-trust architecture adoption. |

|

By vertical application, Financial Services is the dominant vertical in the Software-as-a-Service market, representing approximately USD 30.8 billion in 2025. Healthcare is the fastest-growing vertical SaaS category, expanding at a CAGR of 17.6% from 2026 to 2035, driven by telehealth platform adoption, EHR digitization, and life sciences workflow automation. |

|

By customer size, Enterprise organizations represent the largest revenue segment of the Software-as-a-Service market at approximately USD 142.0 billion in 2025. The Midmarket segment is the fastest-growing customer tier at a CAGR of 15.9% from 2026 to 2035, as expanded partner-led and marketplace distribution channels make enterprise-grade SaaS accessible to mid-sized buyers. |

|

By deployment model, Public Multi-Tenant architecture dominates the Software-as-a-Service market, accounting for approximately USD 220.0 billion in 2025. Private Cloud deployment is the fastest-growing model at a CAGR of 16.4% from 2026 to 2035, driven by regulated-industry demand for dedicated single-tenant environments meeting data sovereignty requirements. |

|

By commercial model, Seat-Based subscriptions command the largest revenue share in the Software-as-a-Service market at approximately USD 157.8 billion in 2025. Usage-Based commercial models are the fastest-growing at a CAGR of 17.2% from 2026 to 2035, reflecting enterprise preference for aligning software costs directly with consumption volumes across AI-powered workflows. |

|

By distribution channel, Direct Sales remains the largest channel in the Software-as-a-Service market at approximately USD 157.8 billion in 2025. Marketplace distribution is the fastest-growing channel at a CAGR of 18.6% from 2026 to 2035, as AWS Marketplace, Azure Marketplace, and Google Cloud Marketplace enable procurement through existing hyperscaler committed spend. |

|

North America holds the largest regional share of the Software-as-a-Service market at USD 149.3 billion in 2025, forecast to reach USD 530.3 billion by 2035 at a CAGR of 13.5%, anchored by the world's highest enterprise SaaS spend concentration and the headquarters of all major SaaS platform vendors. |

|

Asia-Pacific is the fastest-growing major region in the Software-as-a-Service market at a CAGR of 17.2%, advancing from USD 60.8 billion in 2025 to USD 301.2 billion by 2035, propelled by India's cloud-first enterprise SaaS adoption, China's domestic SaaS ecosystem expansion, and rapid digital transformation across Southeast Asian SMBs. |

|

The United States is the single largest country market in the Software-as-a-Service market, representing approximately 80% of North American revenue in 2025, underpinned by the world's deepest enterprise SaaS vendor ecosystem, highest per-employee SaaS spend, and most advanced AI-native software adoption rates among global buyers. |

|

India is the fastest-growing national market in Asia-Pacific within the Software-as-a-Service market at a CAGR of 21.5% from 2026 to 2035, propelled by the government's Digital India initiative, rapidly expanding startup ecosystem, and the growing domestic SaaS export industry targeting global enterprise buyers. |

Key Emerging Trends in the Software-as-a-Service Market

How Is Generative AI Integration Transforming the Software-as-a-Service Market?

Generative AI is the most consequential technology trend reshaping the Software-as-a-Service market, with virtually every major SaaS vendor embedding AI assistants, copilots, and natural language interfaces into existing product suites. From our research, we found that Microsoft's Copilot integration across Microsoft 365, Dynamics 365, and GitHub, combined with Salesforce Einstein GPT embedded in its CRM suite, signals a structural shift toward AI-augmented SaaS workflows as the new baseline. This transformation drives both premium upsell opportunities and competitive displacement, compelling established and emerging SaaS vendors to accelerate AI roadmap investments or risk losing enterprise renewal contracts to AI-native competitors.

How Is the Rise of Vertical SaaS Reshaping Industry-Specific Software Adoption?

Vertical SaaS platforms purpose-built for specific industries, including healthcare, financial services, construction, and logistics, are capturing growing wallet share within the Software-as-a-Service market by delivering deeper workflow integration, regulatory compliance alignment, and sector-specific data models that horizontal platforms cannot efficiently replicate. Based on our market assessment, we observed that platforms such as Veeva Systems in life sciences, Toast in restaurant technology, and Procore in construction have demonstrated that vertical specialization enables higher retention rates, stronger pricing power, and superior land-and-expand dynamics within defined industry ecosystems compared to broader horizontal SaaS competitors.

How Are Usage-Based Commercial Models Disrupting the Traditional SaaS Pricing Paradigm?

Usage-based pricing is emerging as the dominant commercial transformation within the Software-as-a-Service market, enabling vendors to align revenue recognition with actual product consumption rather than fixed seat licenses. Through NMSC's assessment, we found that vendors including Snowflake, Twilio, Datadog, and AWS have demonstrated that consumption-linked models generate superior net dollar retention, lower initial adoption barriers, and more accurate revenue expansion correlated with customer growth. This commercial model shift is compelling seat-based legacy SaaS vendors across CRM, ERP, and collaboration categories to redesign pricing architectures to compete for budget-conscious midmarket and enterprise buyers.

How Is the Platform Consolidation Wave Redefining Competition in the Software-as-a-Service Market?

Accelerating platform consolidation within the Software-as-a-Service market is concentrating enterprise software spend among fewer, larger platform vendors offering integrated suites that reduce procurement complexity, integration overhead, and total cost of ownership. Our findings suggest that Microsoft's expansion from productivity into security, CRM, and DevOps, alongside Salesforce's broadening from CRM into data, marketing, and analytics, reflects a deliberate strategy to capture a larger share of enterprise software budgets through platform consolidation. This trend disadvantages standalone point-solution SaaS vendors while creating margin compression risk for those unable to differentiate through deep vertical integration or AI-native product differentiation.

What Are the Key Market Drivers, Breakthroughs, and Investment Opportunities that Will Shape the Software-as-a-Service Market Industry in the Next Decade?

|

Drivers / Trends / Restraints |

(+/-) % Impact on CAGR Forecast |

Geographic Relevance |

Impact Timeline |

|

Generative AI Integration Across SaaS Suites |

+2.4% |

Global (led by North America, Europe) |

2025–2030 |

|

Cloud-Native Enterprise Digital Transformation |

+1.8% |

North America, Europe, APAC |

2025–2028 |

|

Vertical SaaS Expansion in Healthcare and BFSI |

+1.4% |

Global (all regions) |

2026–2035 |

|

Usage-Based Pricing Model Adoption |

+1.1% |

North America, Europe, Australia |

2025–2032 |

|

Marketplace Distribution Channel Growth |

+0.9% |

North America, Europe |

2025–2030 |

|

SMB and Midmarket SaaS Penetration |

+0.8% |

APAC, LATAM, MEA |

2026–2035 |

|

Data Privacy and Sovereignty Compliance Complexity |

-1.1% |

Europe, APAC, North America |

Ongoing |

|

Cybersecurity Risk and SaaS Sprawl Management |

-0.7% |

All regions |

Ongoing |

|

Rising Customer Acquisition Costs Amid Competition |

-0.5% |

North America, Europe |

2025–2028 |

|

AI-Native SaaS Startups Disrupting Legacy Vendors |

+1.6% |

Global |

2026–2035 |

|

Public Sector FedRAMP and Compliance Opportunities |

+0.7% |

North America, MEA, APAC |

2025–2035 |

What Are the Growth Drivers of the Software-as-a-Service Market?

How Is Global Enterprise Digital Transformation Driving Demand in the Software-as-a-Service Market?

Enterprise digital transformation represents the most sustained structural demand driver across the broader SaaS industry. Organizations across every sector are migrating on-premises software estates to cloud-delivered SaaS platforms to reduce operational overhead, accelerate IT modernization, and enable distributed workforce productivity. Based on NMSC's research, we found that the U.S. federal government's Cloud Smart Strategy, overseen by the General Services Administration and the Office of Management and Budget, has allocated sustained annual investment into cloud software adoption, expanding the public-sector SaaS addressable market significantly. This institutional digitization trend extends across European government cloud programs, India's Digital India initiative, and Saudi Arabia's Vision 2030 technology modernization roadmap.

How Is Generative AI Embedding Creating Recurring Upsell Revenue in the Software-as-a-Service Market?

The embedding of generative AI capabilities within existing SaaS platforms is creating a powerful incremental revenue layer within the Software-as-a-Service market. Vendors are introducing AI add-on modules priced above baseline seat fees, generating premium subscription tiers that expand average revenue per user across installed customer bases. Our analysis shows that Microsoft's Copilot for Microsoft 365, priced at a premium above standard subscriptions, and Salesforce's Einstein AI tier represent documented commercial strategies for AI-driven ARPU expansion. The U.S. National Institute of Standards and Technology's AI Risk Management Framework establishes governance standards that further formalize AI software adoption within compliance-sensitive enterprise environments.

How Does the Global SMB Digitization Wave Expand the Software-as-a-Service Market's Total Addressable Market?

The ongoing digitization of small and medium businesses globally is materially expanding the total addressable market of the Software-as-a-Service market by bringing millions of previously underserved organizations into the cloud software subscription economy. Affordable, mobile-first SaaS tools for accounting, payroll, CRM, and project management are enabling SMBs across Asia-Pacific, Latin America, and Africa to deploy enterprise-grade capabilities at consumer price points. NMSC's analysis indicates that India's Ministry of Micro, Small, and Medium Enterprises has actively promoted cloud software adoption through technology upgrade schemes, creating structured government-backed demand for SMB-focused SaaS platforms within the world's largest small business economy.

What Are the Growth Inhibitors of the Software-as-a-Service Market?

How Does Cross-Jurisdictional Data Privacy Regulation Constrain Software-as-a-Service Market Expansion?

Regulatory fragmentation across jurisdictions represents a material structural constraint on the Software-as-a-Service market, particularly for vendors seeking to serve regulated industries and government clients across multiple geographies simultaneously. The EU's GDPR and the EU AI Act, together with U.S. state-level privacy laws including California's CPRA and Virginia's CDPA, impose conflicting data handling, consent, and residency requirements that increase compliance engineering costs and extend enterprise procurement cycles. From our assessment, we observed that the U.S. Government Accountability Office has documented how compliance complexity increases the time and cost of cloud software procurement across federal agencies, a pattern mirrored in private-sector regulated industry procurement globally.

How Does SaaS Sprawl and Integration Complexity Limit Further Penetration in the Software-as-a-Service Market?

As enterprise organizations have accumulated large SaaS application portfolios over the past decade, SaaS sprawl has emerged as a significant adoption inhibitor within the Software-as-a-Service market. Organizations struggle to govern, integrate, secure, and extract value from fragmented software estates comprising dozens or hundreds of cloud applications. Our findings suggest that integration complexity raises total cost of ownership, increases cybersecurity exposure through unmanaged API connections, and drives executive resistance to adding further SaaS subscriptions without demonstrable ROI. The U.S. Cybersecurity and Infrastructure Security Agency has issued guidance on SaaS application security risks, elevating this challenge to a formal national cybersecurity concern that affects procurement decisions at large enterprise and government buyers.

What Are the Growth Opportunities in the Software-as-a-Service Market?

How Does the Public Sector FedRAMP and Government Cloud Adoption Create a Structural Opportunity in the Software-as-a-Service Market?

Government cloud adoption programs represent a significant and structurally durable growth opportunity within the Software-as-a-Service market. The U.S. Federal Risk and Authorization Management Program (FedRAMP), administered by the General Services Administration, has established a structured marketplace for government-authorized cloud software products that provides vendors with simultaneous access to the multi-hundred-billion-dollar federal IT procurement market. Through our market evaluation, we assessed that FedRAMP-authorized SaaS vendors benefit from a protected competitive moat within the public sector, where authorization serves as a prerequisite rather than a differentiator. Similar frameworks in Europe, Singapore, and Australia are creating comparable structured SaaS opportunities in government markets globally.

How Does the Vertical SaaS Specialization Opportunity in Healthcare and Life Sciences Represent a High-Growth Pathway?

Healthcare and life sciences represent the highest-conviction vertical SaaS opportunity within the Software-as-a-Service market, driven by systemic underinvestment in health IT digitization across developing and developed markets alike. The U.S. Department of Health and Human Services' 21st Century Cures Act mandates interoperability and data exchange standards that compel healthcare provider organizations to adopt compliant SaaS platforms for EHR access, patient engagement, and claims management. NMSC's analysis indicates that the global expansion of telehealth, AI-assisted diagnostics, and payer-provider data exchange creates durable multi-decade demand for healthcare-specific SaaS platforms across both regulated and high-growth emerging market healthcare systems.

How Does AI-Native SaaS Innovation Create New Market Categories Within the Software-as-a-Service Ecosystem?

The emergence of AI-native SaaS companies building products designed from the ground up for generative AI workflows, rather than retrofitting AI onto legacy architectures, is creating entirely new product categories within the Software-as-a-Service market. From our research, we found that AI-native SaaS platforms for legal workflow automation, clinical documentation, code generation, and financial analysis are capturing enterprise budget previously allocated to consulting services, custom software development, and manual knowledge worker processes. The NIST AI Risk Management Framework and emerging EU AI Act compliance requirements create parallel demand for AI governance and explainability SaaS tools, representing an additional emerging category within the broader SaaS taxonomy.

How Is the Software-as-a-Service Market Segmented in This Report, and What Are the Key Insights from the Segmentation Analysis?

Segmentation Analysis Overview

This Software-as-a-Service market report analyzes the market across six primary segmentation dimensions: Application, Customer Size, Deployment Model, Commercial Model, Distribution Channel, and Geography. The analysis below presents key findings from each segment.

How Do Horizontal SaaS Applications Dominate Revenue Across the Software-as-a-Service Market?

|

Horizontal Application Segment |

2025 (USD Bn) |

2035 (USD Bn) |

CAGR (%) |

|

CRM and Customer Service |

38.4 |

131.8 |

13.1% |

|

Marketing and Commerce |

28.6 |

102.4 |

13.6% |

|

ERP and Finance |

32.2 |

118.6 |

13.9% |

|

Human Capital Management |

24.8 |

91.2 |

13.9% |

|

Accounting and Tax |

14.4 |

52.8 |

13.9% |

|

Collaboration and Productivity |

31.6 |

116.4 |

13.9% |

|

Content and Agreements |

12.2 |

46.2 |

14.2% |

|

IT Service Management |

10.8 |

42.6 |

14.7% |

|

Workflow and Automation |

8.6 |

37.4 |

15.8% |

|

Communications and Telephony |

12.4 |

44.2 |

13.6% |

|

Analytics and BI |

18.8 |

78.6 |

15.4% |

|

Security and Identity |

14.2 |

68.4 |

17.0% |

|

Developer Tools and DevOps |

8.4 |

38.2 |

16.3% |

|

Observability and Monitoring |

5.2 |

26.8 |

17.8% |

|

Other Horizontal |

3.2 |

10.8 |

12.9% |

Based on our analysis of enterprise software investment trends, horizontal SaaS applications represent the dominant category within the Software-as-a-Service market, covering CRM and Customer Service, ERP and Finance, Human Capital Management, Collaboration and Productivity, Security and Identity, Analytics and BI, and multiple other cross-industry application categories. From our market assessment, we observed that CRM and Customer Service, including Sales Automation, Customer Support, and Customer Data Platform sub-segments, commands the largest share due to universal enterprise demand for customer relationship and revenue management tools. Security and Identity is the fastest-growing horizontal category, encompassing Identity and Access Management, Endpoint Protection, Cloud Security, Threat Detection, and GRC, driven by escalating enterprise cybersecurity investment across all geographies. Analytics and BI, incorporating Reporting, Visualization, Planning, and Data Platform services, is also experiencing above-average growth as organizations invest in self-service intelligence capabilities embedded within cloud workflows.

Which Industry Verticals Are Driving the Fastest Growth in the Software-as-a-Service Market?

|

Vertical Application Segment |

2025 (USD Bn) |

2035 (USD Bn) |

CAGR (%) |

|

Financial Services |

30.8 |

112.4 |

13.8% |

|

Healthcare |

18.6 |

88.2 |

16.8% |

|

Retail and Commerce |

14.4 |

56.6 |

14.7% |

|

Manufacturing and Supply Chain |

11.8 |

44.2 |

14.1% |

|

Education |

7.6 |

30.8 |

15.0% |

|

Public Sector |

6.8 |

26.4 |

14.6% |

|

Other Verticals |

4.6 |

16.8 |

13.8% |

Our assessment of vertical SaaS adoption patterns indicates that the Software-as-a-Service market's vertical application segment spans Financial Services, Healthcare, Retail and Commerce, Manufacturing and Supply Chain, Education, Public Sector, and Other Verticals including Legal, Construction, Energy, Telecommunications, Transportation, Professional Services, and Media. Financial Services, covering Banking, Insurance, and Wealth Management SaaS platforms, commands the largest vertical share due to regulatory compliance requirements, high per-user software budgets, and sophisticated analytics and risk management demands across global financial institutions. Healthcare is the fastest-growing vertical at a CAGR of 16.8%, encompassing Provider, Payer, and Life Sciences SaaS platforms benefiting from telehealth expansion, interoperability mandates, and AI-assisted clinical workflow adoption globally. Education, covering K-12, Higher Education, and Corporate Training SaaS platforms, is also growing strongly as institutions worldwide digitize learning management and administrative workflows.

How Does Customer Size Influence SaaS Adoption Patterns and Revenue Distribution?

|

Customer Size Segment |

2025 (USD Bn) |

2035 (USD Bn) |

CAGR (%) |

|

Enterprise |

142.0 |

492.4 |

13.2% |

|

Midmarket |

82.6 |

325.8 |

14.8% |

|

Small Business |

56.4 |

228.6 |

15.0% |

|

Consumer and Prosumer |

34.6 |

201.0 |

19.3% |

From our research, we found that this industry is segmented into Enterprise, Midmarket, Small Business, and Consumer and Prosumer customer tiers, each representing distinct product requirements, procurement patterns, and growth trajectories. The Enterprise segment dominates due to large multi-seat, multi-product SaaS deployments across Microsoft, Salesforce, SAP, Workday, and ServiceNow platforms, with multi-year enterprise agreements generating predictable recurring revenue at scale. Midmarket is the fastest-growing enterprise customer segment as expanded partner-led, marketplace, and self-service channels lower procurement friction. Consumer and Prosumer is the highest CAGR segment overall at 19.3%, driven by the rapid adoption of AI-powered creative, productivity, and personal finance SaaS tools.

How Do Deployment Architecture Preferences Shape the Software-as-a-Service Market's Competitive Landscape?

|

Deployment Model |

2025 (USD Bn) |

2035 (USD Bn) |

CAGR (%) |

|

Public Multi-Tenant |

220.0 |

742.2 |

12.9% |

|

Dedicated Single Tenant |

38.4 |

164.6 |

15.6% |

|

Private Cloud |

36.8 |

182.4 |

17.4% |

|

Hybrid |

20.4 |

158.6 |

22.7% |

Based on NMSC's research, the Software-as-a-Service market is segmented by deployment model into Public Multi-Tenant, Dedicated Single Tenant, Private Cloud, and Hybrid architectures. Public Multi-Tenant dominates due to its lower cost structure, shared infrastructure efficiency, and alignment with the majority of standard enterprise SaaS deployments across productivity, CRM, and collaboration categories. Private Cloud deployment is growing rapidly as regulated industries including banking, insurance, defense, and healthcare require isolated SaaS environments meeting data sovereignty and audit requirements. Hybrid deployment is the fastest-growing model at a CAGR of 22.7%, reflecting enterprise demand for architectures that bridge on-premises systems with cloud-native SaaS applications through integrated data and identity management frameworks.

How Are Evolving Commercial Models Reshaping Revenue Dynamics in the Software-as-a-Service Market?

|

Commercial Model |

2025 (USD Bn) |

2035 (USD Bn) |

CAGR (%) |

|

Seat Based |

157.8 |

498.6 |

12.2% |

|

Usage Based |

68.4 |

312.8 |

16.4% |

|

Transaction Based |

34.6 |

152.4 |

15.9% |

|

Hybrid |

28.2 |

148.6 |

18.1% |

|

Freemium and Ad-Supported |

26.6 |

135.4 |

17.6% |

Our analysis of SaaS commercial model evolution indicates that the Software-as-a-Service market operates across Seat-Based, Usage-Based, Transaction-Based, Hybrid, and Freemium and Ad-Supported pricing architectures. Seat-Based remains the largest commercial model due to its prevalence across established enterprise SaaS categories including Microsoft 365, Salesforce, Workday, and ServiceNow. Usage-Based is the fastest-growing traditional model as AI-intensive workloads, API-driven software consumption, and communications platforms favor pay-per-use pricing that aligns vendor revenue with demonstrated customer value delivery. Hybrid commercial models, combining base seat fees with consumption-linked expansion, are emerging as the dominant structure for AI-augmented SaaS suites seeking to monetize incremental AI usage beyond baseline subscriptions.

Which Distribution Channels Are Reshaping Go-to-Market Strategies in the Software-as-a-Service Market?

|

Distribution Channel |

2025 (USD Bn) |

2035 (USD Bn) |

CAGR (%) |

|

Direct Sales |

157.8 |

487.6 |

11.9% |

|

Partner Led |

78.8 |

299.4 |

14.3% |

|

Self-Service |

42.2 |

198.6 |

16.8% |

|

Marketplace |

24.4 |

172.4 |

21.5% |

|

OEM Embedded |

12.4 |

89.8 |

21.9% |

Through NMSC's assessment, we found that the Software-as-a-Service market distributes product through Direct Sales, Partner-Led, Self-Service, Marketplace, and OEM Embedded channels, each serving distinct buyer personas and deal structures. Direct Sales remains the dominant channel for enterprise accounts requiring customized implementation, dedicated customer success support, and multi-year contract negotiation. Marketplace is the fastest-growing channel in this segment at a CAGR of 21.5%, as AWS Marketplace, Azure Marketplace, and Google Cloud Marketplace enable streamlined procurement through committed cloud spend agreements. OEM Embedded distribution, where SaaS capabilities are integrated within third-party products and platforms, is growing at 21.9% CAGR as software vendors license capabilities for white-label embedding into industry-specific solutions.

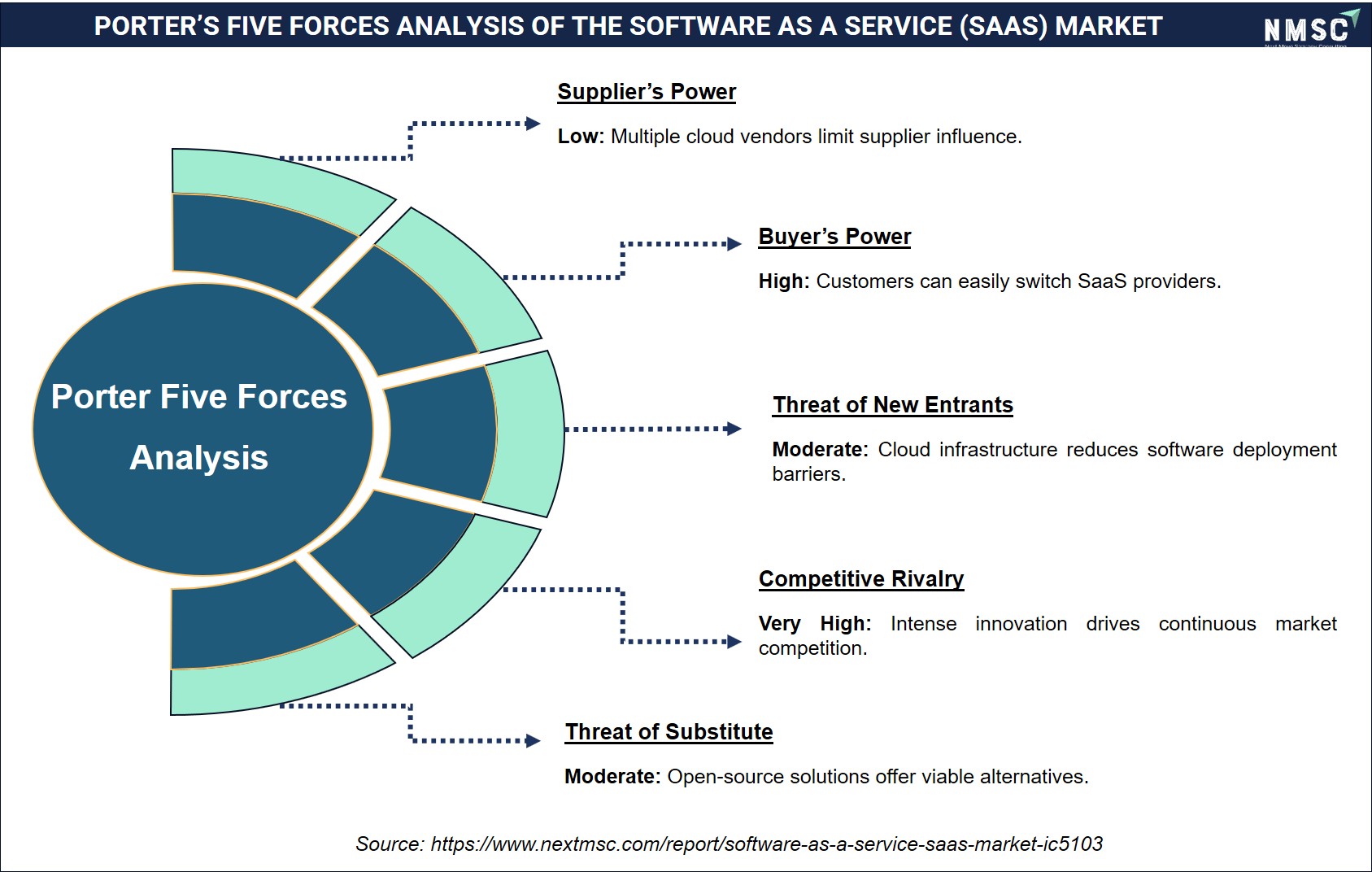

Porter's Five Forces Analysis of the Software-as-a-Service Market

The Porter's Five Forces analysis highlights the competitive dynamics shaping the Software-as-a-Service (SaaS) market. Competitive rivalry is high due to the presence of numerous global and niche providers competing through innovation, pricing, and feature differentiation. The threat of new entrants remains moderate, supported by cloud infrastructure accessibility but constrained by brand reputation and customer acquisition costs. Buyer bargaining power is high, as customers can easily compare alternatives and switch providers. Supplier power is moderate, driven by dependence on cloud infrastructure and technology vendors. The threat of substitutes is also moderate, with on-premise software and custom-built solutions serving as alternatives, encouraging continuous product enhancement and customer-focused innovation.

Regional Outlook

Regional Revenue and Growth Summary 2025–2035

|

Region |

2025 (USD Bn) |

2035 (USD Bn) |

CAGR (%) |

Key Driver |

|

North America |

149.3 |

530.3 |

13.5% |

Enterprise AI spend, vendor HQ concentration |

|

Europe |

78.6 |

274.4 |

13.3% |

GDPR compliance, public-sector SaaS programs |

|

Asia-Pacific |

60.8 |

301.2 |

17.2% |

India cloud-first enterprise, China SaaS growth |

|

Middle East & Africa |

12.8 |

67.6 |

18.1% |

Vision 2030, digital economy programs |

|

Latin America |

14.1 |

74.3 |

18.1% |

Digital transformation, SMB SaaS adoption |

North America Software-as-a-Service Market

North America is the global epicenter of the market, holding the largest Software-as-a-Service market share globally and contributing USD 149.3 billion in 2025, forecast to reach USD 530.3 billion by 2035 at a CAGR of 13.5%. The region benefits from the headquarters of all leading SaaS platform vendors, the world's highest enterprise SaaS spend per employee, and a mature cloud adoption infrastructure supporting rapid AI integration across horizontal and vertical SaaS categories. The U.S. federal government's cloud-first digital strategy and FedRAMP-authorized procurement marketplace further sustain public-sector SaaS demand, reinforcing North America's structural market leadership across the forecast period.

U.S. Software-as-a-Service Market

Based on our engagements across enterprise software procurement trends, the United States represents over 80% of North American Software-as-a-Service market revenue and is the world's single largest national SaaS market. The U.S. benefits from the highest concentration of Fortune 500 enterprise SaaS buyers, the headquarters of Microsoft, Salesforce, Adobe, Oracle, ServiceNow, Workday, CrowdStrike, Snowflake, and Palo Alto Networks, and a venture-backed startup ecosystem generating continuous AI-native SaaS innovation. The General Services Administration's FedRAMP program and the U.S. Department of Defense's cloud adoption mandate have created a multi-billion-dollar government SaaS procurement channel supporting sustained demand throughout the forecast period.

Canada Software-as-a-Service Market

Through our analysis, Canada represents approximately 12% of North American Software-as-a-Service market revenue. Canadian financial institutions, insurance companies, and public-sector organizations are sophisticated enterprise SaaS buyers investing in cloud productivity, security, and analytics platforms. The Government of Canada's Digital Ambition and Cloud Adoption Strategy have accelerated public-sector SaaS spending, while Canadian enterprises are increasingly evaluating Canadian-region sovereign cloud deployments from AWS, Azure, and Google Cloud. Data sovereignty considerations around the U.S. CLOUD Act influence procurement decisions, driving demand for Canadian-hosted SaaS and government-grade data residency configurations within the Software-as-a-Service market.

Mexico Software-as-a-Service Market

From our assessment, Mexico is the fastest-growing market within North America in the Software-as-a-Service market, expanding at a CAGR of 18.4% from 2026 to 2035. Mexico's dynamic fintech ecosystem, expanding manufacturing sector serving global supply chains, and nearshoring investment wave from Asia are generating enterprise demand for ERP, supply chain, and HR SaaS platforms. The government's National Digital Strategy and public-sector cloud modernization initiatives are expanding SaaS procurement beyond the private sector. Mexico's Ley Federal de Protección de Datos Personales is driving compliance-oriented SaaS investment within this national market.

Europe Software-as-a-Service Market

Europe is the second-largest region in the Software-as-a-Service market, contributing USD 78.6 billion in 2025 and forecast to reach USD 274.4 billion by 2035 at a CAGR of 13.3%. Europe's regulatory environment, anchored by GDPR, the EU AI Act, the Digital Markets Act, and the EU Data Act, is simultaneously a structural demand driver for compliance-oriented SaaS and a complexity factor increasing time-to-procurement. Sovereign cloud investment, led by GAIA-X and national digital transformation programs across Germany, France, and Italy, creates a structurally differentiated market environment for compliant SaaS vendors within this regional market.

UK Software-as-a-Service Market

Based on our engagements across European enterprise SaaS markets, the United Kingdom is Europe's largest individual Software-as-a-Service market, representing approximately 22% of European revenue in 2025. Post-Brexit, the UK maintains GDPR-equivalent standards through UK GDPR while gaining regulatory flexibility attracting technology investment. The Financial Conduct Authority's Open Finance initiative and HM Treasury's fintech strategy are creating demand for financial services SaaS platforms. London's status as a global financial hub drives strong enterprise SaaS spend across CRM, risk management, compliance automation, and analytics categories within this national market.

Germany Software-as-a-Service Market

According to our evaluation, Germany is Europe's second-largest Software-as-a-Service market, driven by its world-class manufacturing and industrial sector's adoption of ERP, supply chain, and industrial IoT SaaS platforms. German enterprises maintain among the strictest data privacy procurement requirements globally, demanding GDPR-compliant SaaS deployments with EU data residency. SAP's enterprise application dominance in the German market provides a structural advantage for SAP-adjacent SaaS vendors. The Federal Office for Information Security cloud certification framework shapes vendor compliance requirements within this national market.

France Software-as-a-Service Market

Through our analysis, France represents Europe's third-largest Software-as-a-Service market, characterized by strong public-sector digital transformation investment and national AI strategy commitments under France 2030. The French government's cloud computing strategy prioritizes sovereign cloud solutions, benefiting EU-headquartered SaaS vendors and compliant hyperscaler regional deployments. The CNIL, France's data protection authority, enforces GDPR rigorously, compelling organizations to invest in privacy-compliant SaaS architectures. French enterprises in banking, insurance, and defense are significant buyers of security, identity, and compliance SaaS platforms within the France Software-as-a-Service market.

Italy Software-as-a-Service Market

From our assessment, Italy is a growing mid-tier Software-as-a-Service market, with expanding adoption across financial services, manufacturing, and public administration. The Italian government's Piano Nazionale di Ripresa e Resilienza (PNRR) has directed substantial investment toward cloud migration for public-sector entities, creating structured demand within this national market. The Polo Strategico Nazionale provides a national strategic cloud supporting sovereign SaaS deployment for government agencies. Italy's Garante data protection authority actively enforces GDPR compliance, driving investment in governed SaaS governance and data lineage capabilities.

Spain Software-as-a-Service Market

Based on our evaluation, Spain demonstrates growing momentum in the Software-as-a-Service market, driven by a dynamic banking sector, expanding retail ecosystem, and accelerating public-sector digitization under Agenda España Digital 2026. Spanish enterprises in banking, insurance, and telecommunications are significant buyers of CRM, ERP, and security SaaS platforms. The Agencia Española de Protección de Datos enforces GDPR actively, compelling investment in privacy-engineering SaaS tools. AWS, Azure, and Microsoft all operate local cloud regions in Spain, supporting enterprise data residency requirements within this national market.

Sweden Software-as-a-Service Market

Through our market assessment, we observed that Sweden holds one of the highest Software-as-a-Service adoption rates in Europe relative to GDP, reflecting the country's highly digitized economy, strong startup culture, and mature enterprise cloud infrastructure. Swedish enterprises across financial services, retail, telecommunications, and manufacturing are early adopters of AI-augmented SaaS platforms for productivity and analytics. The Swedish Authority for Privacy Protection enforces GDPR diligently, maintaining a high compliance bar within the Sweden Software-as-a-Service market and sustaining demand for security and data governance SaaS solutions.

Denmark Software-as-a-Service Market

From our assessment, Denmark is among the most digitally advanced economies in Europe, with the Danish government's eGovernment strategy and Digital Strategy 2022–2025 supporting high public-sector SaaS adoption. Danish enterprises in shipping, pharmaceutical, and financial services sectors invest significantly in SaaS platforms for supply chain, clinical research, and risk management. The Datatilsynet enforces GDPR standards, maintaining a structured compliance environment within the Denmark Software-as-a-Service market that drives demand for privacy-by-design SaaS architecture.

Finland Software-as-a-Service Market

Based on our engagements, Finland demonstrates strong Software-as-a-Service market adoption driven by a highly educated technology workforce, advanced telecommunications infrastructure, and government leadership in public-sector digital services. Finnish enterprises in technology, healthcare, and manufacturing are active adopters of cloud-native SaaS platforms for collaboration, project management, and DevOps. The Tietosuojavaltuutettu enforces Finland's data protection standards, sustaining compliance-oriented SaaS investment within the Finland Software-as-a-Service market and driving demand for privacy-ready enterprise applications.

Netherlands Software-as-a-Service Market

According to our evaluation, the Netherlands is a strategically important Software-as-a-Service market in Europe, serving as a European headquarters hub for numerous global technology companies and a major regional cloud infrastructure center. Dutch enterprises in financial services, logistics, and agri-food sectors are sophisticated SaaS buyers with high IT investment per employee. The Autoriteit Persoonsgegevens is an active GDPR enforcement authority, reinforcing compliance-led SaaS adoption within this national market. Amsterdam's status as a European data center hub further supports enterprise cloud software procurement.

Rest of Europe Software-as-a-Service Market

The Rest of Europe Software-as-a-Service market encompasses Central and Eastern European countries including Poland, Czech Republic, Romania, and the Baltics, along with Switzerland, Austria, Belgium, and Portugal. NMSC's analysis indicates that CEE markets are experiencing above-European-average growth driven by increasing digital infrastructure investment, growing tech-savvy workforces, and EU digital single market programs that are accelerating enterprise cloud software adoption. Switzerland's financial services sector sustains high-value SaaS demand for banking, compliance, and wealth management platforms. Collectively, the Rest of Europe markets represent a significant and growing contribution to the overall European SaaS industry.

Asia-Pacific Software-as-a-Service Market

Asia-Pacific is the fastest-growing major region in the Software-as-a-Service market, contributing USD 60.8 billion in 2025 and forecast to reach USD 301.2 billion by 2035 at a CAGR of 17.2%. The region's growth is underpinned by India's rapidly expanding domestic SaaS ecosystem, China's large and growing enterprise software market, and accelerating digital transformation across Southeast Asia's high-growth economies. Government-backed digital infrastructure programs, the proliferation of mobile-first cloud software adoption, and rising enterprise AI investment collectively make Asia-Pacific the most dynamically evolving geography within the global SaaS industry.

China Software-as-a-Service Market

From our assessment, China represents the largest Software-as-a-Service market in Asia-Pacific in absolute revenue terms. China's enterprise SaaS ecosystem is dominated by domestic platforms including Alibaba Cloud, Tencent Cloud, and ByteDance's Lark collaboration suite, which compete with localized offerings from global vendors navigating China's data residency and cybersecurity laws. The Cyberspace Administration of China's Data Security Law and Personal Information Protection Law mandate stringent data localization requirements, structurally favoring domestic SaaS vendors within this national market and creating distinct barriers for international software providers.

India Software-as-a-Service Market

Based on our engagements, India is the fastest-growing national market in Asia-Pacific within the Software-as-a-Service market at a CAGR of 21.5% from 2026 to 2035. India's SaaS industry serves dual roles as a major domestic consumption market and a globally significant SaaS export hub, with hundreds of India-headquartered SaaS companies serving North American and European enterprise buyers. The Digital India initiative, India Stack infrastructure, and the Digital Personal Data Protection Act create a structured environment for enterprise SaaS adoption. The Ministry of Electronics and Information Technology's cloud adoption programs further expand government demand within the India Software-as-a-Service market.

Japan Software-as-a-Service Market

Through our analysis, Japan is a mature and structurally significant Software-as-a-Service market supported by strong enterprise digitization investment and government-led cloud adoption programs under Japan's Digital Agency, established in 2021. Japanese enterprises in manufacturing, retail, and financial services are transitioning from legacy on-premises systems to cloud SaaS platforms at an accelerating pace. The Personal Information Protection Commission enforces Japan's APPI data protection law, sustaining compliance-led SaaS demand. Japan's government cloud platform for public-sector digitization is expanding structured demand within this national market.

South Korea Software-as-a-Service Market

According to our evaluation, South Korea is an advanced Software-as-a-Service market characterized by high broadband penetration, technologically sophisticated enterprises, and government leadership in digital infrastructure. Korean enterprises in semiconductor, electronics, and financial services sectors invest significantly in ERP, analytics, and security SaaS platforms. The Korea Internet and Security Agency enforces data protection standards, sustaining compliance-oriented SaaS adoption within this national market. Korea's cloud computing promotion law further supports structured enterprise and government SaaS procurement.

Taiwan Software-as-a-Service Market

From our assessment, Taiwan is a technology-intensive Software-as-a-Service market driven by its globally significant semiconductor and electronics manufacturing sector. Taiwanese enterprises increasingly adopt ERP, supply chain, and collaboration SaaS platforms to manage complex global supply chain operations and multinational customer relationships. The government's digital government initiative is expanding public-sector SaaS demand within this national market. Taiwan's Personal Data Protection Act governs enterprise data handling, creating compliance-led demand for privacy-ready SaaS architecture.

Indonesia Software-as-a-Service Market

Based on our engagements, Indonesia represents one of Southeast Asia's most significant Software-as-a-Service growth opportunities, driven by a population of over 270 million, rapidly expanding digital economy, and growing tech-savvy SMB sector. The government's Making Indonesia 4.0 roadmap and national digital transformation programs are accelerating enterprise cloud adoption. Indonesia's Personal Data Protection Law, passed in 2022, is driving investment in compliant SaaS data governance solutions within the Indonesia Software-as-a-Service market. Fintech, e-commerce, and logistics represent the most active vertical SaaS adoption sectors.

Vietnam Software-as-a-Service Market

Through our market assessment, Vietnam is an emerging and fast-growing Software-as-a-Service market benefiting from rapid manufacturing sector digitization, expanding fintech ecosystem, and a young, digitally connected workforce. The Vietnamese government's National Digital Transformation Program targets broad adoption of cloud-based software across government, enterprise, and SMB sectors. Vietnam's Decree 13/2023 on personal data protection is prompting compliance-oriented SaaS investment within the Vietnam Software-as-a-Service market. Foreign direct investment in manufacturing and technology sectors further sustains demand for ERP, HCM, and supply chain SaaS platforms.

Australia Software-as-a-Service Market

From our assessment, Australia is the most mature Software-as-a-Service market in the Asia-Pacific region outside China and India, characterized by high cloud adoption rates, strong enterprise technology budgets, and a sophisticated regulatory environment. The Australian Government's Whole-of-Government Cloud Strategy and ASD's Cloud Computing Security for Tenants guidance shape enterprise and public-sector SaaS procurement requirements. The Office of the Australian Information Commissioner enforces the Privacy Act, sustaining compliance-led demand within this national market. Australian enterprises in mining, financial services, and healthcare are leading SaaS adopters.

Philippines Software-as-a-Service Market

According to our evaluation, the Philippines is a strategically growing Software-as-a-Service market driven by its large and expanding business process outsourcing industry, growing domestic enterprise sector, and government digitization programs. The national eGovernment master plan and the Department of Information and Communications Technology's cloud adoption framework are expanding public-sector SaaS procurement. The National Privacy Commission enforces the Data Privacy Act, creating compliance-led demand for security and data governance SaaS solutions within this national market. BPO sector demand for CRM, contact center, and productivity SaaS platforms is particularly strong.

Malaysia Software-as-a-Service Market

Based on our engagements, Malaysia is an advanced Software-as-a-Service market within Southeast Asia, supported by government digital economy programs including MyDIGITAL and a well-developed national cloud computing infrastructure. Malaysian enterprises in financial services, manufacturing, and government are active SaaS adopters, with the Multimedia Development Corporation supporting cloud industry development. Malaysia's Personal Data Protection Act governs enterprise data management, sustaining compliance-oriented SaaS adoption within this national market. Kuala Lumpur is emerging as a regional hub for SaaS vendor operations targeting broader Southeast Asian enterprise markets.

Rest of Asia-Pacific Software-as-a-Service Market

The Rest of Asia-Pacific SaaS landscape encompasses New Zealand, Thailand, Singapore, Bangladesh, Sri Lanka, and other growing economies across the region. Singapore serves as a major regional headquarters hub for global SaaS vendors and a high-value enterprise market in its own right, supported by the Monetary Authority of Singapore's technology risk guidelines and the government's Smart Nation digital transformation agenda. New Zealand maintains high SaaS adoption rates driven by a cloud-forward government strategy. Collectively, the Rest of APAC markets represent a growing and diversified contribution to the global Software-as-a-Service market.

Middle East and Africa Software-as-a-Service Market

The Middle East and Africa Software-as-a-Service market contributed USD 12.8 billion in 2025 and is forecast to reach USD 67.6 billion by 2035 at a CAGR of 18.1%, representing one of the most dynamic growth regions globally. Gulf Cooperation Council economies led by Saudi Arabia and the UAE are executing large-scale digital economy programs that are driving enterprise SaaS procurement across government, financial services, and healthcare. African markets, particularly Nigeria and South Africa, are experiencing growing SaaS adoption among fintech startups and enterprise buyers investing in cloud infrastructure alternatives to expensive legacy on-premises systems.

Saudi Arabia Software-as-a-Service Market

From our assessment, Saudi Arabia is the largest and fastest-growing Software-as-a-Service market in the Middle East, driven by Vision 2030's comprehensive digital economy transformation agenda. The Saudi Authority for Data and Artificial Intelligence and the National Data Management Office are creating structured frameworks for SaaS procurement across government and regulated industries. Saudi Arabia's cloud-first government initiative, Etimad platform for public digital services, and large-scale smart city programs in NEOM are generating significant and growing enterprise SaaS demand within the this national market.

UAE Software-as-a-Service Market

Based on our engagements, the UAE is a highly sophisticated Software-as-a-Service market, serving as the Middle East's leading technology hub with hyperscaler cloud regions from AWS, Azure, and Google Cloud all operating UAE-based data centers. Dubai's Smart City initiative, ADGM regulatory sandbox, and the UAE's National AI Strategy drive enterprise SaaS adoption across financial services, logistics, and government sectors. The UAE's Personal Data Protection Law governs SaaS data handling requirements, sustaining compliance-led investment within this national market. The UAE is also a significant launchpad for SaaS vendors expanding across the broader Middle East region.

Egypt Software-as-a-Service Market

Through our analysis, Egypt is the largest Software-as-a-Service market in North Africa, driven by government digital transformation programs under Egypt's Digital Egypt strategy and expanding enterprise cloud adoption across the country's large banking, telecommunications, and retail sectors. Egypt's large young population, growing internet penetration, and increasing mobile-first digital service adoption are expanding the addressable SMB SaaS market. The Ministry of Communications and Information Technology actively promotes cloud technology investment, creating structured incentives for enterprise SaaS adoption within this national market.

Israel Software-as-a-Service Market

According to our evaluation, Israel is a globally significant Software-as-a-Service market and innovation hub, home to a disproportionately large concentration of cybersecurity, AI-native SaaS, and enterprise software startups relative to its population. Israeli SaaS companies including Monday.com, WalkMe, and Wix serve global enterprise and SMB markets, establishing Israel as both a SaaS producer and consumer economy. The Israeli Privacy Protection Authority oversees data governance, sustaining compliance-led SaaS demand within this national market. Israel's defense and intelligence sector creates specialized demand for security-grade SaaS platforms.

Turkey Software-as-a-Service Market

From our assessment, Turkey is a mid-tier Software-as-a-Service market experiencing growing enterprise cloud adoption driven by the country's large manufacturing base, rapidly expanding e-commerce sector, and government digitization programs. Turkey's large young population and expanding startup ecosystem are creating domestic demand for SaaS tools across productivity, CRM, and analytics categories. The Personal Data Protection Authority enforces Turkey's KVKK data protection law, compelling compliance-led SaaS investment within the Turkey Software-as-a-Service market. Several global SaaS vendors have established regional offices in Istanbul to address the broader Eastern Europe and Middle East enterprise market.

Nigeria Software-as-a-Service Market

Based on our engagements, Nigeria is Sub-Saharan Africa's largest Software-as-a-Service market, driven by the continent's most dynamic fintech ecosystem, a large and growing internet-connected population, and rapid digitization across the financial services, retail, and telecommunications sectors. The Nigerian government's digital economy strategy and the National Information Technology Development Agency's cloud adoption framework support enterprise SaaS procurement. The Nigeria Data Protection Commission enforces the Nigeria Data Protection Act, creating structured compliance requirements within this national market. Mobile-first SaaS delivery models are particularly well-suited to Nigeria's connectivity landscape.

South Africa Software-as-a-Service Market

Through our analysis, South Africa is the most mature Software-as-a-Service market in Sub-Saharan Africa, with a well-established enterprise cloud adoption base across financial services, mining, retail, and government. South Africa's Department of Public Service and Administration cloud strategy and the Government IT Officers Council framework support public-sector SaaS procurement. The Information Regulator enforces POPIA, South Africa's data protection law, sustaining compliance-oriented SaaS investment within this national market. Johannesburg serves as the primary regional operations hub for global SaaS vendors serving the broader southern and eastern African enterprise market.

Rest of MEA Software-as-a-Service Market

The Rest of Middle East and Africa Software-as-a-Service market encompasses Bahrain, Kuwait, Oman, Qatar, Jordan, Kenya, Ghana, Morocco, and other growing economies across the region. Gulf Cooperation Council markets outside Saudi Arabia and the UAE are implementing National Vision programs with significant cloud software investment components. East African markets, particularly Kenya, are experiencing above-regional-average SaaS growth driven by leading fintech adoption, strong mobile money infrastructure, and an active startup ecosystem. Morocco is emerging as North Africa's second-largest SaaS market supported by government-backed digital transformation initiatives.

Latin America Software-as-a-Service Market

Latin America is among the fastest-growing regions in the Software-as-a-Service market, contributing USD 14.1 billion in 2025 and forecast to reach USD 74.3 billion by 2035 at a CAGR of 18.1%. The region's growth is driven by Brazil's large enterprise technology market, rapid fintech and e-commerce expansion across major economies, and increasing SMB digitization supported by affordable mobile-first SaaS platforms. Government-backed digital transformation programs in Brazil, Mexico, Colombia, and Chile are expanding public-sector SaaS procurement and creating structured demand across this regional market.

Brazil Software-as-a-Service Market

Based on our engagements, Brazil is Latin America's largest Software-as-a-Service market, accounting for approximately 45% of regional revenue in 2025. Brazil's large enterprise economy, dynamic fintech ecosystem, and government-driven digital transformation programs are sustaining strong SaaS demand. The Autoridade Nacional de Proteção de Dados enforces Brazil's LGPD data protection law, compelling enterprise investment in privacy-compliant SaaS architectures within this national market. AWS, Microsoft Azure, and Google Cloud operate Brazilian cloud regions, supporting data residency requirements for enterprise and government SaaS buyers.

Argentina Software-as-a-Service Market

From our assessment, Argentina is a significant Software-as-a-Service market within Latin America, supported by a skilled technology workforce, growing startup ecosystem, and increasing enterprise cloud adoption. Despite macroeconomic volatility, Argentina's technology sector demonstrates sustained SaaS growth, particularly in B2B productivity, CRM, and analytics platforms serving domestic and international clients. The Agencia de Acceso a la Información Pública oversees data protection standards within this national market, driving compliance-led SaaS investment. Argentina's SaaS export industry is also growing as locally headquartered vendors serve North American and European markets.

Chile Software-as-a-Service Market

Through our analysis, Chile is the most advanced Software-as-a-Service market in terms of digital infrastructure maturity within the southern cone of Latin America. Chile's Digital Agenda and government cloud adoption strategy have accelerated public-sector SaaS procurement, while the country's sophisticated financial services and mining sectors sustain strong enterprise demand. The Consejo para la Transparencia oversees data protection, and Chile's new Data Protection Law aligns with international privacy standards within this national market, driving investment in compliant cloud software platforms.

Colombia Software-as-a-Service Market

According to our evaluation, Colombia is a rapidly growing Software-as-a-Service market driven by digital transformation investment across the financial services, retail, and government sectors. The Colombian government's Digital Colombia agenda and MinTIC's cloud adoption framework are expanding public-sector SaaS procurement. Bogotá is emerging as a regional hub for SaaS vendor operations in the Andean market. The Superintendencia de Industria y Comercio enforces data protection standards within this national market, creating compliance-led demand for privacy-ready enterprise SaaS platforms.

Rest of Latin America Software-as-a-Service Market

The Rest of Latin America SaaS landscape encompasses Peru, Ecuador, Venezuela, Central America, and the Caribbean. Peru and Ecuador are experiencing growing enterprise SaaS adoption driven by expanding financial services digitization and government cloud programs. Central American markets, including Costa Rica, Panama, and Guatemala, benefit from proximity to North American enterprise buyers and active nearshore technology services industries sustaining SaaS tool demand. Collectively, the Rest of LATAM markets are growing at above-regional-average rates, representing a meaningful incremental opportunity within the global Software-as-a-Service market.

Competitive Landscape

Competitive Dynamics and M&A Landscape

|

Key Takeaways |

Details |

|

Market Structure |

Highly fragmented at the long tail, with platform concentration among a small number of hyperscale vendors. Microsoft, Salesforce, Adobe, SAP, and Oracle collectively represent a significant share of enterprise SaaS revenue through multi-product platform strategies. |

|

Innovation Focus |

Generative AI integration, usage-based pricing expansion, vertical SaaS specialization, and platform ecosystem consolidation. Vendors embedding AI copilots, automated workflow generation, and natural language interfaces across existing product suites are creating premium upsell opportunities. |

|

M&A Activity |

Active consolidation with platform vendors acquiring point-solution SaaS companies to expand product surface area. Notable activities include Salesforce's acquisition of Own Company for data protection, CrowdStrike's ecosystem expansion through security acquisitions, and ServiceNow's integration of AI-native workflow automation platforms. |

How Do Companies Compete in the Software-as-a-Service Market?

Competition in the Software-as-a-Service market is characterized by multi-dimensional rivalry spanning platform breadth, AI capability depth, pricing model flexibility, and ecosystem integration. NMSC's analysis indicates that dominant platform vendors including Microsoft, Salesforce, and ServiceNow compete through suite consolidation, offering customers unified platforms that reduce integration complexity and total cost of ownership relative to multi-vendor point-solution portfolios. Mid-tier and specialist SaaS vendors compete through vertical depth, product-led growth, and self-service acquisition models that bypass traditional enterprise sales cycles. Pricing strategy differentiation, ranging from usage-based consumption to freemium-led conversion, is emerging as a primary competitive lever across this industry.

Which Kind of Companies Dominate the Software-as-a-Service Market?

The market is dominated by large platform vendors capable of offering integrated multi-product suites covering CRM, ERP, security, collaboration, and analytics within unified ecosystems. Microsoft's cross-platform strategy spanning Microsoft 365, Azure, Dynamics 365, GitHub, and Security products represents the most comprehensive SaaS portfolio in the market. Salesforce's Customer 360 platform, Adobe's Creative and Experience Cloud suite, and SAP's Business Suite demonstrate that SaaS leadership increasingly requires multi-cloud, multi-product depth that sustains high enterprise switching costs and enables revenue expansion through AI-augmented upsell layers within the Software-as-a-Service market.

AI-Native Differentiation and Open Standards Drive Market Success in the Software-as-a-Service Market

AI-native differentiation is becoming a primary determinant of competitive positioning within the Software-as-a-Service market as enterprises evaluate SaaS renewals and new purchases. Our findings suggest that vendors with deeply integrated, proprietary AI capabilities built on large-scale training data, including Microsoft Copilot trained on enterprise Microsoft 365 data and Salesforce Einstein built on CRM interaction history, command meaningful pricing premiums and improved renewal rates. Simultaneously, open-standard API architectures and ecosystem interoperability are becoming baseline procurement requirements, as enterprise buyers resist proprietary lock-in in favor of composable SaaS architectures enabling multi-vendor flexibility.

Market Players to Opt for Merger and Acquisition Strategies to Expand Their Presence in the Software-as-a-Service Market

Merger and acquisition activity remains a primary growth strategy within the SaaS industry as established platform vendors seek to expand product surface area, acquire AI capabilities, enter new verticals, and neutralize emerging competitive threats. From our research, we found that the Software-as-a-Service market has experienced sustained M&A activity with platform vendors selectively acquiring AI-native startups in security, analytics, and workflow automation to supplement organic development. Private equity investment in SaaS buy-and-build strategies continues to consolidate fragmented point-solution markets in categories including legal tech, construction tech, and healthcare SaaS, creating new integrated vertical platforms within the SaaS industry.

Who Are the Key Market Players in the Software-as-a-Service Market?

-

Microsoft Corporation

-

Salesforce, Inc.

-

Adobe Inc.

-

SAP SE

-

Oracle Corporation

-

Intuit Inc.

-

ServiceNow, Inc.

-

Palo Alto Networks, Inc.

-

Workday, Inc.

-

Autodesk, Inc.

-

Atlassian Corporation

-

Zoom Video Communications, Inc.

-

CrowdStrike Holdings, Inc.

-

Snowflake Inc.

-

Datadog, Inc.

-

HubSpot, Inc.

-

DocuSign, Inc.

-

Zscaler, Inc.

-

Okta, Inc.

-

RingCentral, Inc.

What Are the Latest Developments in the Software-as-a-Service Market Industry?

|

Date |

Event |

|

Feb 2026 |

Salesforce announced rapid adoption of Agentforce IT Service, with more than 180 organizations replacing legacy ITSM systems, reinforcing its SaaS leadership in AI-powered workflow automation. |

|

Jan 2026 |

Microsoft acquired Osmos, an agentic AI data-engineering platform, to strengthen Microsoft Fabric and autonomous data engineering capabilities. This expands Microsoft's SaaS analytics and data platform portfolio. |

|

Oct 2025 |

Adobe expanded its partnership with Google Cloud, integrating Gemini, Veo, and Imagen AI models into Adobe's SaaS creative ecosystem. |

Expert Insights

“A lot of the business logic will move to a new tier, which then will be a multi-agent tier that needs to be orchestrated. It's going to be an agent that will orchestrate across multiple SaaS applications,”

“A lot of the business logic will move to a new tier, which then will be a multi-agent tier that needs to be orchestrated. It's going to be an agent that will orchestrate across multiple SaaS applications,”

— Satya Nadella, Chairman & CEO, Microsoft

Statement made during an interview discussing the impact of AI agents on enterprise software architecture and the future evolution of Software-as-a-Service (SaaS) platforms (January 2025).

Market Interpretation

The comment highlights a fundamental shift occurring within the Software-as-a-Service (SaaS) market as artificial intelligence becomes increasingly integrated into enterprise software ecosystems. Nadella suggests that AI-powered agents will emerge as a new orchestration layer capable of managing workflows across multiple SaaS applications, reducing the need for users to interact with individual software systems separately. This evolution is expected to accelerate demand for interoperable SaaS platforms, open APIs, unified data architectures, and intelligent automation capabilities. As organizations seek greater productivity and streamlined operations, SaaS providers are increasingly investing in agentic AI, workflow automation, and cross-platform integration, positioning AI-enabled orchestration as a key driver of future market growth and competitive differentiation.

What Are the Investment Opportunities in the Software-as-a-Service Market?

Capital Inflows and Venture Activity

The Software-as-a-Service (SaaS) Market continues to attract substantial private and institutional investment, driven by recurring revenue models, strong cash flow visibility, and the growing integration of artificial intelligence into enterprise software platforms. Major funding rounds, including investments in AI-native SaaS companies and enterprise automation platforms, have reinforced investor confidence in the sector's long-term growth prospects. We observed that publicly traded SaaS leaders such as Salesforce, ServiceNow, HubSpot, Snowflake, and Datadog continue to command significant market valuations, while venture capital activity remains robust across emerging categories including AI-powered productivity software, vertical SaaS solutions, cybersecurity SaaS, and customer experience platforms. According to industry venture funding trends, enterprise software and AI-related SaaS solutions represented a substantial share of global technology investments during 2024 and 2025, reflecting sustained confidence in cloud-based business applications.

Cloud Infrastructure and Platform Investment

Cloud infrastructure investment remains a critical growth enabler for the Software-as-a-Service (SaaS) Market. Global hyperscale cloud providers continue to expand data center capacity and AI infrastructure to support increasing SaaS adoption across industries. Furthermore, Microsoft announced plans to invest approximately USD 80 billion in AI-optimized data centers in fiscal year 2025, while Alphabet committed approximately USD 75 billion in capital expenditure focused primarily on cloud and AI infrastructure expansion. These investments enhance the scalability, reliability, and performance of SaaS applications while enabling advanced AI-driven capabilities such as generative AI assistants, intelligent automation, and predictive analytics. Expanding cloud infrastructure also supports global SaaS deployment and reduces operational costs for software vendors serving enterprise customers.

ESG and Sustainable Cloud Operations

Environmental, Social, and Governance (ESG) considerations are increasingly influencing investment decisions within the Software-as-a-Service (SaaS) Market. As organizations seek to reduce the environmental impact of their IT operations, cloud-based SaaS solutions are often viewed as more resource-efficient alternatives to on-premises software deployments. Regulatory initiatives, including the European Union's sustainability directives and government-led carbon reduction programs, are encouraging enterprises to prioritize environmentally responsible technology vendors. Major cloud providers continue to pursue ambitious sustainability goals, including renewable energy sourcing, carbon reduction initiatives, and energy-efficient data center operations. SaaS providers that demonstrate strong ESG performance, transparent reporting practices, and sustainable cloud architectures are increasingly favored by enterprise customers and institutional investors.

Digital Transformation and Enterprise Modernization

Software as a Service platforms play a foundational role in enterprise digital transformation initiatives, positioning the market as a long-term beneficiary of global technology modernization spending. Organizations undertaking ERP modernization, customer experience transformation, workforce digitization, cybersecurity upgrades, and business process automation increasingly rely on SaaS applications to improve agility and operational efficiency. We further analyzed that government and industry digital transformation frameworks across North America, Europe, and Asia-Pacific continue to emphasize cloud adoption, data-driven decision-making, and enterprise software modernization as key drivers of economic competitiveness. As a result, SaaS vendors are positioned to benefit from multi-year technology investment cycles across both public and private sectors.

Private Equity and Strategic M&A Activity

Private equity firms continue to deploy significant capital across the Software-as-a-Service ecosystem, targeting high-growth software vendors, industry-specific SaaS providers, cybersecurity platforms, and workflow automation companies. Leading investment firms such as Vista Equity Partners, Thoma Bravo, Silver Lake, and Bain Capital have remained active participants in software-focused acquisitions and platform investments. Strategic mergers and acquisitions are also accelerating as established software vendors seek to expand capabilities in artificial intelligence, workflow automation, cybersecurity, customer engagement, and industry-specific cloud applications. We assessed that investors should closely monitor consolidation opportunities in AI-powered SaaS, vertical SaaS platforms, cybersecurity software, collaboration tools, and intelligent automation solutions, which are expected to remain among the most attractive investment segments within the Software-as-a-Service (SaaS) Market during the 2026–2028 period.

Key Benefits for Stakeholders

For Enterprise Buyers

Enterprise buyers gain comprehensive, vendor-neutral insights into the Software-as-a-Service (SaaS) Market, including quantitative market sizing across application categories, deployment models, organization sizes, and industry verticals. This intelligence supports software procurement planning, cloud transformation initiatives, vendor selection, and long-term digital modernization strategies. Our competitive landscape analysis enables decision-makers to benchmark leading SaaS vendors, compare subscription models, evaluate total cost of ownership (TCO), and make informed build-versus-buy decisions for mission-critical business applications with greater confidence and strategic clarity.

For Investors and Financial Analysts

Investors and financial analysts receive a structured, data-driven assessment of the Software-as-a-Service (SaaS) Market's growth outlook, competitive landscape, merger and acquisition activity, and segment-level revenue forecasts through 2035. Detailed CAGR analysis across application segments, deployment environments, enterprise sizes, and regional markets supports investment evaluation, portfolio optimization, and valuation modeling. Comprehensive profiles of leading SaaS providers, combined with tracking of strategic partnerships, product innovations, acquisitions, and funding activities, provide valuable insights for identifying emerging growth leaders, acquisition opportunities, and competitive risks within the global SaaS ecosystem.

For SaaS Vendors and Software Providers

SaaS vendors and software providers gain actionable intelligence on high-growth market opportunities, competitive positioning gaps, customer demand trends, and emerging technology adoption patterns within the Software-as-a-Service (SaaS) Market. Application-level analysis highlights attractive growth areas such as AI-powered software, cybersecurity SaaS, workflow automation, customer experience platforms, industry-specific vertical SaaS, and collaborative productivity solutions. Regional market assessments identify geographic expansion opportunities while considering cloud adoption maturity, regulatory environments, and digital transformation readiness. The analysis of customer segments, pricing strategies, and distribution channels enables vendors to optimize go-to-market approaches, strengthen customer acquisition strategies, improve retention, and maximize recurring revenue growth.

For Government and Regulatory Bodies